UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 40-F

|

o

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2010

|

Commission File Number: 1-31349

|

THOMSON REUTERS CORPORATION

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant's name into English (if applicable))

Province of Ontario, Canada

(Province or other jurisdiction of incorporation or organization)

2741

(Primary Standard Industrial Classification Code Number (if applicable))

98-0176673

(I.R.S. Employer Identification Number (if applicable)

3 Times Square, New York, New York 10036

Telephone: (646) 223-4000

(Address and telephone number of Registrant's principal executive offices)

Thomson Reuters Holdings Inc.

Attn: Deirdre Stanley, Executive Vice President and General Counsel

3 Times Square

New York, New York 10036

Telephone: (646) 223-4000

(Name, address (including zip code) and telephone number (including area code) of agent for service in the United States)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|

Common shares

|

New York Stock Exchange

|

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Debt Securities

For annual reports, indicate by check mark the information filed with this Form:

|

x Annual information form

|

ý Audited annual financial statements

|

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report:

833,396,235 common shares, 6,000,000 Series II preference shares and 1 Thomson Reuters Founders Share

Indicate by check mark whether the Registrant by filing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934 (the "Exchange Act"). If "Yes" is marked, indicate the file number assigned to the Registrant in connection with such Rule.

| Yes o 82-_________ |

No x

|

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

|

Yes x

|

No o

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

|

Yes o

|

No o

|

UNDERTAKING AND CONSENT TO SERVICE OF PROCESS

a. Undertaking.

The Registrant undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an annual report on Form 40-F arises; or transactions in said securities.

b. Consent to Service of Process.

|

|

(1)

|

The Registrant has previously filed a Form F-X in connection with the class of securities in relation to which the obligation to file this report arises.

|

|

|

(2)

|

Any change to the name or address of the Registrant’s agent for service shall be communicated promptly to the Commission by amendment to Form F-X referencing the file number of the Registrant.

|

SIGNATURES

Pursuant to the requirements of the Exchange Act, the Registrant certifies that it meets all of the requirements for filing on Form 40-F and has duly caused this annual report to be signed on its behalf by the undersigned, thereto duly authorized.

|

THOMSON REUTERS CORPORATION

|

||

|

By:

|

/s/ Deirdre Stanley

|

|

|

Name:

|

Deirdre Stanley

|

|

|

Title:

|

Executive Vice President and General Counsel

|

|

|

Date: March 9, 2011

|

EXHIBIT INDEX

|

Exhibit Number

|

|

Description

|

|

|

Annual Report for the year ended December 31, 2010 (which constitutes an Annual Information Form and includes Management’s Discussion and Analysis and Audited Financial Statements for the year ended December 31, 2010), and includes a Form 40-F Cross Reference Table on page 148

|

|

|

|

Consent of PricewaterhouseCoopers LLP

|

|

|

|

Certification of the Chief Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002

|

|

|

|

Certification of the Chief Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002

|

|

|

|

Certification of the Chief Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002

|

|

|

|

Certification of the Chief Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002

|

|

|

|

Audit Committee Charter

|

Exhibit 99.1

ANNUAL REPORT 2010

MARCH 9, 2011

|

|

|

Information in this annual report is provided as of March 1, 2011, unless otherwise indicated.

Certain statements in this annual report are forward-looking. These forward-looking statements are based on certain assumptions and reflect our current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Some of the factors that could cause actual results to differ materially from current expectations are discussed in the “Risk Factors” section of this annual report as well as in materials that we from time to time file with, or furnish to, the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission. There is no assurance that any forward-looking statements will materialize. You are cautioned not to place undue reliance on forward-looking statements, which reflect expectations only as of the date of this annual report. Except as may be required by applicable law, we disclaim any intention or obligation to update or revise any forward-looking statements.

The following terms in this annual report have the following meanings, unless otherwise indicated:

|

|

—

|

“Thomson Reuters,” “we,” “us” and “our” each refers to Thomson Reuters Corporation and its consolidated subsidiaries, unless the context otherwise requires;

|

|

|

—

|

“Woodbridge” refers to The Woodbridge Company Limited and other companies affiliated with it; and

|

|

|

—

|

“$,” “US$” or “dollars” are to U.S. dollars.

|

For information regarding our disclosure requirements under applicable Canadian and U.S. laws and regulations, please see the “Cross Reference Tables” section of this annual report.

Information contained on our website or any other websites identified in this annual report is not part of this annual report. All website addresses listed in this annual report are intended to be inactive, textual references only. The Thomson Reuters logo and our other trademarks, trade names and service names mentioned in this annual report are the property of Thomson Reuters.

TABLE OF CONTENTS

|

2

|

Business

|

|

18

|

Risk Factors

|

|

23

|

Management’s Discussion and Analysis

|

|

74

|

Consolidated Financial Statements

|

|

133

|

Executive Officers and Directors

|

|

139

|

Additional Information

|

|

147

|

Cross Reference Tables

|

Thomson Reuters Annual Report 2010

1

BUSINESS

OVERVIEW

We are the leading source of intelligent information for the world’s businesses and professionals, providing customers with competitive advantage. Intelligent information is a unique synthesis of human intelligence, industry expertise and innovative technology that provides decision-makers with the knowledge to act, enabling them to make better decisions faster. Through over 55,000 employees across more than 100 countries, we deliver this must-have insight to the financial, legal, tax and accounting, healthcare, science and media markets, powered by the world’s most trusted news organization.

We are organized in two divisions:

|

|

●

|

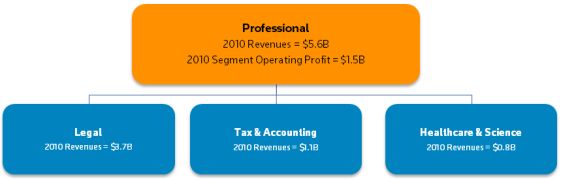

Professional, which consists of our legal, tax and accounting, healthcare and science businesses; and

|

|

|

●

|

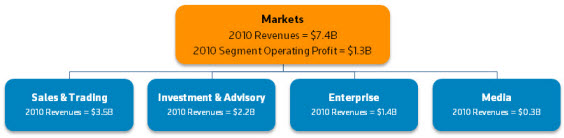

Markets, which consists of our financial and media businesses.

|

BUSINESS MODEL AND KEY OPERATING CHARACTERISTICS

We serve a wide variety of customers with a single, tested business model. We derive the majority of our revenues from selling electronic content and services to professionals, primarily on a subscription basis. The table below describes some of our key operating characteristics.

|

Industry leader

|

●

|

#1 or #2 in most of the market segments that we serve

|

|

|

Balanced and diversified

|

●

|

Five distinct core customer groups

|

|

|

●

|

Geographical diversity – our revenues in 2010 were 59% from the Americas, 30% from Europe, the Middle East and Africa (EMEA) and 11% from Asia

|

||

|

●

|

Our largest single customer accounts for approximately 1% of revenues

|

||

|

Attractive business model

|

●

|

86% of our 2010 revenues were recurring

|

|

|

●

|

Strong and consistent cash flow generating abilities

|

||

|

Strong technology platforms and valuable content

|

●

|

Proprietary databases and deeply embedded workflow tools and solutions

|

|

|

●

|

91% of our 2010 revenues were from information delivered electronically, software and services

|

||

|

Reuters acquisition and legacy savings program benefits

|

●

|

Substantial cost savings from acquisition and operational improvements, which have exceeded initial targets

|

|

|

Disciplined financial policies

|

●

|

Invest to drive long-term growth and returns

|

|

|

●

|

Focus on free cash flow

|

||

|

●

|

Support business objectives with a robust capital strategy

|

Thomson Reuters Annual Report 2010

2

2010 ACCOMPLISHMENTS

In 2010, our two key strategic objectives were growth and efficiency. While we are proud of what we accomplished in 2010, we are aware that more remains to be done and we are focused on accelerating the pace of change. Last year, we further integrated our operations, strengthened essential infrastructure and launched major new product platforms. The following table provides information about our progress against last year’s priorities.

|

2010 Priorities

|

2010 Progress | ||

|

Growth

|

We returned to revenue growth in the second half of the year. In 2010, we continued investing in growth initiatives and we launched a number of major new product platforms, including: | ||

| ● |

WestlawNext, our next generation legal research platform;

|

||

| ● |

Thomson Reuters Eikon, our new flagship financial information platform which incorporates the innovative Reuters Insider multimedia news service;

|

||

| ● |

ONESOURCE, our global tax workstation;

|

||

| ● |

Advantage Suite 5.0, our redesigned, state-of-the-art tools to support healthcare decision making; and

|

||

| ● |

Thomson Reuters Elektron, an ultra-low latency infrastructure for electronic trading and data distribution.

|

||

| We acquired a number of key foundational assets to support new initiatives. We invested approximately $0.9 billion in the acquisition of companies that included Complinet to support our new Governance, Risk and Compliance (GRC) business; Point Carbon for our Commodities & Energy business; Serengeti, Pangea3, Canada Law Book and Revista dos Tribunais in Legal for Global General Counsel; GeneGo for Life Sciences; and Aegisoft in Sales & Trading. | |||

| We continued to target rapidly developing economies (RDEs) that we believe will be major contributors to future global growth. | |||

|

Efficiency

|

We made significant progress on a number of efficiency and capability-enhancing initiatives, including: | ||

| ● | Consolidating and integrating technology platforms to achieve cost savings and increase flexibility and scalability; | ||

| ● | Transforming the technology infrastructure of our data centers through standardization, virtualization and automation; and | ||

| ● | Rolling out new customer administration platforms, including a consolidated order-to-cash system which will streamline our interaction with customers and provide us with better usage data. | ||

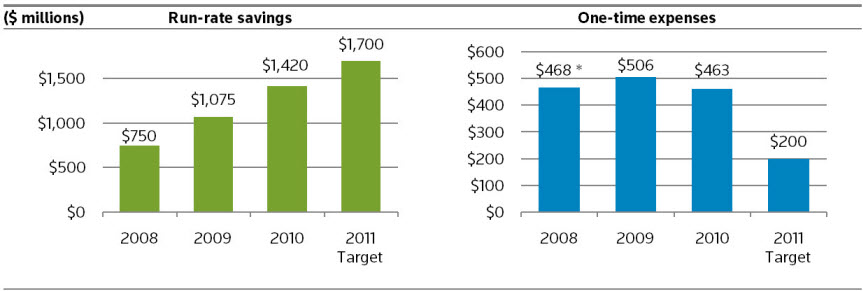

| Our Reuters integration plus legacy savings initiatives achieved approximately $1.4 billion of annualized run-rate savings as of the end of 2010. | |||

In 2010, we returned to revenue growth. We were able to raise our growth targets during the year as the markets began to improve, and we ended the year with good momentum.

|

|

●

|

Our 2010 revenues from ongoing businesses before currency were $13.1 billion;

|

|

|

●

|

Revenue growth before currency was 1%;

|

|

|

●

|

Our underlying operating profit margin was 19.6% (20.0% before currency and acquisitions); and

|

|

|

●

|

Our underlying free cash flow, which enables us to keep investing in the business and pay dividends, was $2.0 billion.

|

Our new investments in product launches and acquisitions contributed to a 7% decline in underlying operating profit. However, our period of heavy investment is now nearly completed.

Thomson Reuters Annual Report 2010

3

2011 PRIORITIES

In 2011, our top priorities remain focused on growth and efficiency. Our key business activities in 2011 to accelerate growth and capture efficiencies are to:

|

|

—

|

Maximize the growth of our core businesses, such as the U.S. Legal subscription business, Sales & Trading and Investment & Advisory;

|

|

|

—

|

Accelerate our investments in faster growing international markets, with a particular emphasis on rapidly developing economies;

|

|

|

—

|

Reallocate investment to faster growing segments of our business, such as Governance, Risk & Compliance and Commodities & Energy; and

|

|

|

●

|

Streamline product lines, consolidate platforms, reduce technology costs and accelerate the sharing of information across the corporation.

|

PROFESSIONAL DIVISION

The Professional division consists of our businesses in the Legal, Tax & Accounting and Healthcare & Science sectors. In 2010, the Professional division launched a number of new products, focused on global expansion outside of the United States and achieved net savings through efficiency initiatives.

LEGAL

Legal is a leading provider of critical information, decision support tools, software and services to legal, intellectual property (IP), compliance, business and government professionals around the world. Legal offers a broad range of products and services that utilize our electronic databases of legal, regulatory, news and business information. These products and services include legal research solutions, software-based workflow solutions, compliance solutions, marketing, finance and operations technology and consulting services and legal process outsourcing services.

Westlaw is Legal’s primary online delivery platform. Westlaw offers authoritative content, powerful search and collaboration features and navigation tools that enable customers to find and share specific points of law, build tables of authorities and search for topically-related commentary. In 2010, Legal launched WestlawNext in the United States. WestlawNext delivers improved search, research organization and new collaboration capabilities. We believe these capabilities help researchers get answers faster and provide higher quality, more cost efficient advice.

Thomson Reuters Annual Report 2010

4

In 2010, we launched country-specific versions of Westlaw in India and Hong Kong. We also provide versions of Westlaw for legal professionals in Canada, Chile, China, Ireland, Japan, Spain, the United Kingdom and other countries. Legal also has country-specific online legal research services, some of which are sold under brand names other than Westlaw, including services in Argentina, Australia, Brazil, Denmark, France, New Zealand, Sweden and the United Kingdom. In 2010, Legal acquired Revista dos Tribunais, a leading provider of legal research services in Brazil, and plans to launch a new online service this year.

Through Westlaw International, we offer our online products and services to customers in markets where we may not have an existing publishing presence or have not yet developed a fully customized Westlaw service. As of December 31, 2010, Westlaw International was used by practitioners in 65 countries.

Westlaw Litigator is a complete workflow solution that assists lawyers with all phases of litigation by combining relevant legal research materials with practical tools and services for case evaluation, pre-trial investigation, e-discovery, expert witness selection, settlement negotiation and trial preparation and presentation.

Legal also has a leading collection of assets that support IP lawyers and business professionals across the IP lifecycle, from ideation and maintenance to protection and commercialization.

Legal also is a leading provider of educational information, textbooks and solutions to law students, librarians and professors in the United States. West LegalEdcenter offers one of the largest online collections of continuing legal education (CLE) programs.

In 2010, Legal formed a new Governance, Risk and Compliance (GRC) business unit following the acquisition of Complinet, a leading provider of global compliance information solutions for financial services institutions. The new GRC business unit also includes a number of other Thomson Reuters assets. GRC connects business transactions, strategy and operations to the ever-changing regulatory environment for firms in highly regulated markets.

In 2010, Legal’s acquisitions also included Serengeti, a provider of electronic billing and matter management software, and Pangea3, a leading provider of legal process outsourcing services. Both of these acquisitions expand Legal’s position in the general counsel market, and also complement our existing legal offerings.

The following table provides information about Legal’s major brands.

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

West

WestlawNext

Westlaw

Westlaw Business

Complinet

|

Legal, regulatory and compliance information-based products and services

|

Lawyers, law students, law librarians and other legal professionals

|

||

|

Foundation Press

West Law School Publishing

West LegalEdcenter

|

Textbooks, study aids, continuing education materials and seminars

|

Law students, lawyers and legal professionals

|

||

|

Sweet & Maxwell

Aranzadi

Brookers

La Ley

Lawtel

Revista dos Tribunais

Canada Law Book

|

Legal information-based products and services

|

Lawyers, law students, law librarians, corporate legal professionals, government agencies and trademark professionals

|

Thomson Reuters Annual Report 2010

5

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Carswell

|

Legal, regulatory and compliance information-based products and services

|

Lawyers, law students, law librarians and other legal professionals

|

||

|

Thomson CompuMark

SAEGIS

|

Trademark research and protection

|

Trademark attorneys and agents

|

||

|

Derwent World Patents Index

Thomson Innovation

|

Patent research and analysis

|

Legal, intellectual property, research & development and business professionals

|

||

|

Thomson IP Management Services

|

Intellectual asset management

|

Legal and intellectual property professionals

|

||

|

Elite

Elite 3E

ProLaw

|

Suite of software applications that assist with front- and back-office management functions, including document management, case management, general ledger accounting, timekeeping, billing and records management

|

Lawyers, law firm finance and operations

|

||

|

FindLaw

Hubbard One

|

Online legal directory, website creation and hosting services and law firm marketing solutions

|

Lawyers and legal professionals

|

||

|

Hildebrandt Baker Robbins

|

Strategic, technology, operations and information consulting advisory services

|

Lawyers and law firm finance, operations and business development professionals

|

||

|

Westlaw Litigator

West Case Notebook

West LiveNote

Westlaw CaseLogistix

Westlaw Round Table Group

|

Online research tools, case analysis software, deposition technology, as well as expert witness and document review services to support each stage of the litigation workflow

|

Lawyers, paralegals, courts and court reporters

|

||

|

Serengeti

|

Electronic billing and matter management software

|

Corporate counsel and law firm professionals

|

||

|

Pangea3

|

Legal process outsourcing services

|

Corporate and law firm legal professionals

|

||

|

CLEAR

PeopleMap

|

Public records products and services

|

Government, law enforcement, legal and corporate investigative professionals

|

COMPETITION

Legal’s primary global competitors are Reed Elsevier (which operates LexisNexis) and Wolters Kluwer. Legal also competes with other companies that provide legal and regulatory information, as well as practice and matter management software, client development and other services to support legal professionals.

TAX & ACCOUNTING

Tax & Accounting is a leading global provider of technology and information solutions, as well as integrated tax compliance and accounting software and services, to accounting, tax and corporate finance professionals in accounting firms, corporations, law firms and government. Tax & Accounting has two global businesses – Workflow & Service Solutions and Business Compliance & Knowledge Solutions.

Workflow & Service Solutions provides tax compliance, accounting and practice management software solutions to corporate tax departments and accounting firms around the world.

Business Compliance & Knowledge Solutions provides tax and accounting research and guidance information, online media and CPA certification services to corporations, accounting firms and law firms around the world.

In 2010, Tax & Accounting began to execute its strategy to expand globally, which included launching the ONESOURCE global tax workstation. Tax & Accounting’s global expansion strategy also extends to content research and certification, including plans to offer its flagship product Checkpoint in more countries around the world, and plans to grow several online products and authoritative information for tax and accounting professionals outside the U.S., with brands such as Carswell in Canada, Brookers in New Zealand and La Ley in Argentina.

Thomson Reuters Annual Report 2010

6

The following table provides information about Tax & Accounting’s major brands.

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Workflow & Service Solutions

|

||||

|

ONESOURCE

ONESOURCE Workflow Manager

ONESOURCE Income Tax

ONESOURCE Tax Provision

ONESOURCE Transfer Pricing

ONESOURCE Sales & Use Tax

ONESOURCE Property Tax

ONESOURCE Trust Tax

ONESOURCE 1099

|

Global tax workstation that integrates existing global tax compliance software with local tax compliance tools in a growing number of countries and can manage a company’s entire tax workflow – linking global staff, controllers, finance, and even tax advisors and auditors on one system, and provides the solutions needed to handle tax planning, transfer pricing compliance, tax return compliance and global tax reporting needs. The products or services can be sold separately or as a suite

|

Corporate, legal, bank and trust market and large accounting firms

|

||

|

Abacus

|

Suite of products and related business operations that offer corporate income tax software products to customers in Hong Kong, Ireland, The Netherlands, New Zealand and the U.K. and supply VAT compliance software for 19 countries across Europe and Asia-Pacific

|

Corporate tax departments and large accounting firms

|

||

|

PowerTax

|

Software solution that brings together a range of products to help tax professionals in Australia and New Zealand manage corporate tax, trust and property compliance and management reporting

|

Corporate tax departments and large accounting firms

|

||

|

Sabrix

|

Software and related services covering tax requirements for more than 170 countries, which are used to determine, calculate and record sales tax, VAT, excise tax and industry specific taxes

|

Corporate tax departments and large accounting firms

|

||

|

CS Professional Suite

|

Integrated series of software applications that encompass every aspect of a firm's operations, from collecting client data and posting finished tax returns to the ongoing management of engagements and an accountant’s entire practice

|

Small to medium accounting firms

|

||

|

Enterprise Suite

|

Integrated set of solutions covering tax preparation, engagement, practice management and document and workflow management that include GoSystem Tax and GoFileRoom

|

Large accounting firms

|

||

|

Digita

|

Integrated U.K. tax compliance and accounting software and services

|

Accounting firms and corporate tax departments

|

||

|

Business Compliance & Knowledge Solutions

|

||||

|

Checkpoint

|

Integrated platform that includes information-based solutions, expert guidance and workflow tools from various Tax & Accounting products, such as RIA, WG&L and PPC

|

Accounting firms, corporate tax, finance and accounting departments, law firms and governments

|

||

Thomson Reuters Annual Report 2010

7

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Checkpoint Learning

|

Integrated online offering that combines global research, training and certification with course and credit-tracking capability for individuals and large groups, and includes continuing professional education and training solutions from various products such as PPC, PASS Online, GearUp, MicroMash, Reqwired, and AuditWatch

|

Accounting firms and corporate finance, accounting and tax departments

|

||

|

RIA

Paisley

PPC

WG&L

Quickfinder

Brookers Online

Carswell

La Ley

|

Expert guidance and research from around the globe available on the Checkpoint platform or in print

|

Accounting firms, corporate tax, finance and accounting departments, law firms and governments

|

COMPETITION

Tax & Accounting’s primary competitor across all customer segments is Wolters Kluwer (which includes CCH). Other major competitors include Intuit in the professional software and services market, CORPTAX (owned by MLM Information Services) and Vertex in the corporate software and services market. Tax & Accounting also competes with other providers of software and services.

HEALTHCARE & SCIENCE

Our Healthcare & Science business is a leading provider of information, tools, analytics and decision support solutions that help organizations speed scientific discovery and improve healthcare efficiency and quality.

Our healthcare solutions enable hospitals, clinicians, employers, health plans and governments to more effectively manage the cost and quality of their healthcare spending and delivery, improve their market positioning and drive enterprise growth.

Our science solutions provide science professionals in academia, governments and industry with content, technologies and expertise that assist them in all stages of the research and discovery (R&D) cycle, from scientific discovery to product release.

In 2010, Healthcare & Science launched a new version of Advantage Suite.

The following table provides information about Healthcare & Science’s major brands.

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Thomson Reuters Advantage Suite, MarketScan Research Databases and DataProbe

|

Decision support systems, fraud, waste and abuse detection, market intelligence, benchmarking and research for managing the purchase, administration and delivery of healthcare services and benefits

|

Employers, governmental healthcare purchasers, managed care and insurance companies, pharmaceutical companies and health services research providers

|

||

|

Thomson Reuters Micromedex

|

Comprehensive database and solution set of drugs, disease information, medical emergency and poison control procedures, patient education and other relevant clinical, toxicological and environmental health and safety information

|

Physicians, pharmacists, health professionals, pharmaceutical companies, hospitals, poison control centers, corporations, government agencies and insurance companies

|

||

|

CareDiscovery and

ActionOI

|

Performance improvement solutions integrated with analytics and expert services designed to help reduce risk, focus resources and evaluate and manage performance

|

Hospitals and health systems, administrative staff, service line planners, patient safety and quality managers, business development, marketing, and financial and operations managers

|

Thomson Reuters Annual Report 2010

8

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Thomson Reuters Web of Knowledge

|

Comprehensive and integrated platform that includes proprietary Thomson Reuters databases as well as third party-hosted content, editorially selected websites and tools to access, analyze and manage research information

|

Research scientists and scholars, government agencies, research libraries and universities and colleges

|

||

|

Web of Science

|

Comprehensive database providing a source for journal article-cited references and access to abstracted and indexed journals and conference proceedings; available via the Web of Knowledge platform

|

Research scientists and scholars, government agencies, research libraries and universities and colleges

|

||

|

Thomson Reuters Pharma

|

Integrated online platform that delivers pharmaceutical and drug development information, patents, company news, professional meeting reports and other relevant content

|

Pharmaceutical and biotechnology companies

|

||

|

Thomson Reuters Integrity

|

Integrated online platform delivering drug discovery and biomarker content and analytic functionality

|

Pharmaceutical and biotechnology companies, academic centers and research institutes

|

COMPETITION

The principal competitors of Healthcare & Science in the clinical and drug information market are Reed Elsevier and Wolters Kluwer. Within the Healthcare provider market, Premier and The Advisory Board are principal competitors. Within the Payer market, our principal competitor is Ingenix (a division of UnitedHealth Group). Principal competitors in the Life Sciences market are Reed Elsevier, Wolters Kluwer, Informa and Chemical Abstracts Services (CAS). Within the Science and Scholarly Research market, Reed Elsevier and Google Scholar are principal competitors.

Thomson Reuters Annual Report 2010

9

MARKETS DIVISION

The Markets division serves financial services and corporate professionals globally, with Reuters Media serving a broader professional and consumer media market. The Markets division delivers critical information, supporting technology and infrastructure to a diverse set of customers. These solutions are designed to help our customers generate superior returns, improve risk management, increase access to liquidity and create efficient, reliable infrastructures in increasingly global, electronic and multi-asset class markets. Markets customers can access information and analytics through our web-based desktop solutions, datafeeds and mobile applications for a wide range of devices.

The Markets division consists of our Sales & Trading, Investment & Advisory, Enterprise and Media businesses.

SALES & TRADING

Sales & Trading provides a combination of information, community, trading and post-trade connectivity requirements for the trading floor activities of buy-side and sell-side clients in foreign exchange (FX), fixed income and derivatives, equities and other exchange-traded instruments, as well as in the commodities and energy markets.

In 2010, Sales & Trading launched Thomson Reuters Eikon, a new premium desktop product. Thomson Reuters Eikon combines the latest in multimedia and content in a new, easy to use interface. We plan to utilize Thomson Reuters Eikon as the platform for all of our financial desktop products, ultimately replacing Reuters 3000 Xtra, Reuters Trader and other solutions. Thomson Reuters Eikon users are financial markets professionals who require a powerful combination of deep, global, cross-asset news and content combined with sophisticated pre-trade decision-making, communication and trade connectivity tools. Thomson Reuters Eikon also includes Reuters Insider, our new on-demand video service for financial news, content and information. Customers can personalize Reuters Insider to watch and focus directly on what is important to them.

In 2010, Sales & Trading also strengthened its commodities & energy business by acquiring Point Carbon, a provider of trading analytics, news and content for energy and environmental markets. Traders and portfolio managers utilize Point Carbon’s products and services for information on the fluctuating supply, demand and price of gas, electricity and carbon and to develop market strategies. Point Carbon’s information also covers power output and pipeline capacity, global weather forecasts for heat, wind and rain or political events and crises.

Thomson Reuters Annual Report 2010

10

Sales & Trading’s suite of products also allow customers to trade with each other and connect their systems to electronic markets.

The following table provides information about Sales & Trading’s major brands.

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Thomson Reuters Eikon, Reuters 3000 Xtra

|

Premium desktop products providing pre-trade decision-making tools, news, real-time pricing, trading connectivity and collaboration tools

|

Trading professionals, salespeople, brokers and financial analysts

|

||

|

Thomson Reuters Dealing

|

Peer-to-peer conversational trading product primarily related to FX and money markets

|

FX and money market traders, sales desks, hedge funds and voice brokers

|

||

|

Thomson Reuters Matching

|

Electronic FX trade matching system

|

FX traders, sales desks and hedge funds

|

||

|

Tradeweb

|

Global electronic multi-dealer-to-customer marketplace for trading fixed income, derivatives and money market products which connects major investment banks with institutional clients

|

Institutional traders

|

COMPETITION

Sales & Trading information products compete with Bloomberg, SunGard, Telekurs and IDC as well as local, regional and niche competitors ranging from Markit and SuperDerivatives to Quick, Xinhua Finance and Yahoo! Finance. In the electronic trading business, Sales & Trading competes with Fidessa and the large inter-dealer brokers, such as ICAP’s EBS platform. In addition, Sales & Trading competes with single-bank and multi-bank portals such as FXall and MarketAxess.

INVESTMENT & ADVISORY

Investment & Advisory provides information, analytics and workflow solutions that enable effective decision-making and drive performance by its customers in investment management, investment banking, wealth management and corporate services.

Investment & Advisory customers have direct, real-time access to the global, foundational content sets needed for intelligent decision-making, such as fundamentals, estimates, economic indicators, ownership data, broker research, deals data, equity and fixed income data, filings, exchange data, tick history and time series data. Our proprietary sources of content include I/B/E/S, First Call, Worldscope, Datastream, Lipper, StarMine, StreetEvents and Reuters News.

The Investment Management business provides institutional asset management firms and private banking clients with solutions that enable them to manage and execute every phase of the investment decision process. Our integrated solution suite is designed to enable customers to efficiently monitor the markets and perform fundamental and quantitative analysis, portfolio risk and performance analysis and economic forecasting. We also provide a host of reporting solutions that enable our customers to publish their research and market their funds. In addition, our solutions are linked on the back-end, enabling enterprise efficiency and collaboration and communication across the entire research team.

The Investment Banking business provides workflow solutions for investment bankers, advisors, private equity and venture capital professionals, as well as sell-side brokers. We also provide research support to the academic community. Our solutions support the deal-making community by providing the information and research that enables our customers to undertake the detailed analyses and valuations fundamental to their businesses. Investment bankers rely on our news services (such as BreakingViews and publications such as IFR, Buyouts and VCJ) to deliver market insight and new ideas.

Our Wealth Management business provides workflow solutions to the wealth management community, including managers of high net worth investors and private banking professionals. Our front-to-back office solution gives advisors the tools to streamline back office processes and workflows. Our scalable solution sets offer proposal generation, portfolio management, asset allocation, rebalancing, financial planning, alerting, investment selection tools and performance reporting to wealth management professionals.

Thomson Reuters Annual Report 2010

11

Our Corporate Services business provides targeted solutions across key corporate functions, such as investor relations, public relations, corporate communications, corporate development, finance and treasury. With our solutions, companies can access market-moving information and coordinate decision-making. Customers can also gain competitive insight with our institutional-quality information, analytics and tools, and they can benefit from operational and cost efficiencies by consolidating the number of their outside providers. In 2010, the Corporate Services business launched a series of innovative solutions to complement our existing offerings, including Smart Targets and Web Disclosure for Investor Relations (IR) professionals, Thomson ONE Public Relations for Public Relations (PR) professionals, and advanced visual analytics for corporate development and strategy professionals.

The following table provides information about Investment & Advisory’s major brands.

|

Major Brands and Product Categories

|

Type of Product/Service

|

Target Customers

|

||

|

Thomson ONE platform

|

Integrated access to information, analytics and tools delivered within workspaces designed specifically for each target customer’s workflow

|

Portfolio managers, buy-side research analysts and associates, investment bankers, consultants, lawyers, private equity professionals, wealth management and high net worth professionals

Corporate clients including investor relations officers, public relations officers, strategy and research professionals, treasurers and finance professionals

|

||

|

Thomson Reuters Datastream

|

Sophisticated historical time-series analysis that enables the visualization of economic and asset class trends and relationships

|

Economists, strategists, portfolio managers and research analysts

|

||

|

QA Studio and QA Direct

|

Comprehensive data management and analytics solutions for sophisticated quantitative research

|

Quantitative portfolio managers and research analysts

|

||

|

Thomson Reuters Deal

Analytics

|

Screening, targeting, financial and comparable analysis and valuations, pitch book building, M&A league tables

|

Investment bankers and private equity professionals

|

||

|

Thomson Reuters Deals Business Intelligence

|

Analysis and reporting tools for business planning, including performance, market share and targeting

|

Business management and strategy teams in investment banks

|

||

|

SDC Platinum

|

Database for analyzing investment banking and deal trends

|

Investment bankers, consultants, lawyers and private equity professionals

|

||

|

Thomson Reuters Knowledge Direct for Wealth Management

|

Premium content including exchange data, news, company fundamentals, broker research and consensus reports

|

Wealth management professionals and individual investors

|

||

|

BETA Systems

|

Brokerage processing system

|

Retail and institutional wealth management professionals

|

||

|

Lipper

|

Mutual fund information, benchmarking data, performance information and analysis

|

Asset management professionals including fund marketing, sales, product development, performance measurement, financial intermediaries and individual investors

|

||

|

Multimedia Solutions

|

Webcasting solutions and web publishing tools with unique distribution networks and analytics

|

Corporate communications, employee communications, marketing, IR and PR professionals

|

COMPETITION

Investment & Advisory competes with Bloomberg, FactSet, S&P/Capital IQ, Morningstar, SunGard Data Systems, Broadridge Financial Solutions and other companies.

Thomson Reuters Annual Report 2010

12

ENTERPRISE

Enterprise delivers technology and content for the financial markets, which enable firms to efficiently obtain real and non-real time content to make business and trading decisions and meet regulatory requirements.

In 2010, Enterprise launched Thomson Reuters Elektron, a high-speed, resilient financial markets network and hosting environment. Thomson Reuters Elektron allows financial firms of all sizes to trade faster, gain access to electronic pricing data from over 350 exchanges and trading platforms, and interact with each other across a global and resilient infrastructure.

A key component of Thomson Reuters Elektron is our Enterprise Platform, which enables the open exchange of financial data, liquidity and business opportunities between participants in the financial community.

The Enterprise Content business delivers pricing and reference data used by middle and back offices for trade matching and settlement, risk management and analysis and portfolio evaluation. This includes independent, accurate and timely pricing information for 2.5 million fixed income, derivatives instruments and loans.

The combination of our Machine Readable News and Tick History products delivers unique capabilities for the development and back-testing of quantitative and event-based trading and investment strategies.

Our Enterprise business is also one of the largest providers of risk management solutions.

Omgeo, our joint venture with The Depository Trust & Clearing Corporation, automates and streamlines post-trade operations, enabling clients to accelerate the clearing and settlement of trades and reduce counterparty and credit risk.

The following table provides information about Enterprise’s major brands.

|

Major Brands

|

Type of Product/Service

|

Target Customers

|

||

|

Thomson Reuters Elektron

|

High-speed resilient financial markets network and hosting environment

|

Investment banks, asset managers, custodians, liquidity centers and depositories, hedge funds, prime brokers, proprietary traders, inter-dealer brokers, multilateral trading facilities (MTFs), central banks and fund administrators

|

||

|

Thomson Reuters Real Time

|

Real-time datafeeds related to programmatic and automated trading, market and credit risk, instrument pricing and portfolio management and valuations

|

Financial institutions

|

||

|

Thomson Reuters Enterprise Platform

|

Software platform for integrating and distributing real-time and historical financial information

|

Financial institutions

|

||

|

Thomson Reuters Datascope

|

Data delivery platform for non-streaming cross asset class content globally

|

Custodians, banks, insurance companies, fund administrators, pension firms, mutual funds, hedge funds, sovereign funds, underwriters, market makers, accounting firms and government institutions

|

COMPETITION

Enterprise’s real-time data feeds and pricing and reference data offerings compete with Bloomberg, S&P, IDC and Telekurs. In addition, Enterprise’s market data delivery offerings compete with specialty technology providers, exchanges such as NYSE Euronext and large IT vendors such as IBM. Competitors in the risk management sector include SunGard, Algorithmics, Murex, Misys and Calypso. In the portfolio accounting market, competitors include Eagle, Simcorp Dimension, PAM, Beauchamp and DST.

MEDIA

Powered by approximately 3,000 journalists reporting from nearly 200 bureaus around the world, Media provides indispensable news and information tailored for media and business professionals and drives decision-making around the globe with speed, accuracy and independence.

Our News Agency business provides the world’s media companies with text, video, pictures, graphics and multimedia products.

Thomson Reuters Annual Report 2010

13

In 2010, Media launched Reuters America for Publishers as part of its planned transformation from a traditional news agency business model to a platform-oriented business model that focuses on providing coverage, content solutions and services that meet our clients’ needs. This new service provides U.S.-based print and online publishers with broader and deeper coverage of U.S. news as well as tools and on-demand services designed to increase efficiency, reduce cost and increase revenues.

Our Consumer Publishing products include the advertising-supported, direct-to-consumer publishing activities of Reuters.com and its global network of websites, mobile services and smartphone applications, online video and electronic out-of-home displays. These products deliver professional-grade news, opinion and analysis to business professionals.

The following table provides information about Media’s major brands.

|

Major Brands and Product Categories

|

Type of Product/Service

|

Target Customers

|

||

|

Reuters America for Publishers

|

Tailored solution providing deeper U.S. domestic coverage, flexible delivery formats and services designed to increase newsroom efficiencies

|

U.S.-based print and online publishers

|

||

|

Text

|

Fast, accurate and extensive coverage of global, regional and national news and events in 20 languages covering general, political, business, financial, entertainment, lifestyle, technology, health, science, sports and human- interest news

|

Newspapers, magazines, television and cable networks, radio stations and websites

|

||

|

Video

|

Live/breaking news and file-based delivery of general, financial, sports, entertainment and lifestyle news videos, as well as access to video archive

|

Television and cable networks, newspapers and websites

|

||

|

Pictures

|

Up-to-the-minute photographs from our global network of over 600 photojournalists and an online picture archive that consists of over four million images covering news, sports, features, entertainment and business

|

Newspapers, magazines, book publishers, websites, creative industry, television and cable networks

|

||

|

Graphics

|

Graphics that enhance information and provide a visual analysis of top world events through news, sports, technical, scientific, business, environmental, economic and financial charts and information graphics

|

Newspapers, magazines, book publishers, websites, creative industry, television and cable networks

|

||

|

Multimedia

|

Prioritized, ready-to-publish online reports, video and picture selections designed for digital platforms

|

Digital platforms including websites and mobile services

|

||

|

Consumer publishing

|

Advertising-supported websites, mobile services and smartphone applications, online video and electronic out-of-home displays

|

Global business professionals

|

COMPETITION

Major global competitors of our News Agency business include the Associated Press, Agence France-Presse, Getty and Bloomberg. Competitors of Media’s consumer products and services include WSJ.com, Bloomberg.com, Forbes.com, CNNMoney and FT.com.

CORPORATE HEADQUARTERS

Our corporate headquarters seeks to foster a group-wide approach to management while allowing the Professional and Markets divisions sufficient operational flexibility to serve their customers effectively. The corporate headquarters’ four primary areas of focus are strategy and capital allocation, technology and innovation, talent management and brand management. The corporate headquarters is also responsible for overall direction on communications, investor relations, tax, accounting, finance, treasury and legal, and administers certain human resources services, such as employee compensation, benefits administration, share plans and training and development.

Thomson Reuters Annual Report 2010

14

Our corporate headquarters are located in New York, New York with key operations in the United Kingdom, India, Eagan, Minnesota and Stamford, Connecticut.

TECHNOLOGY

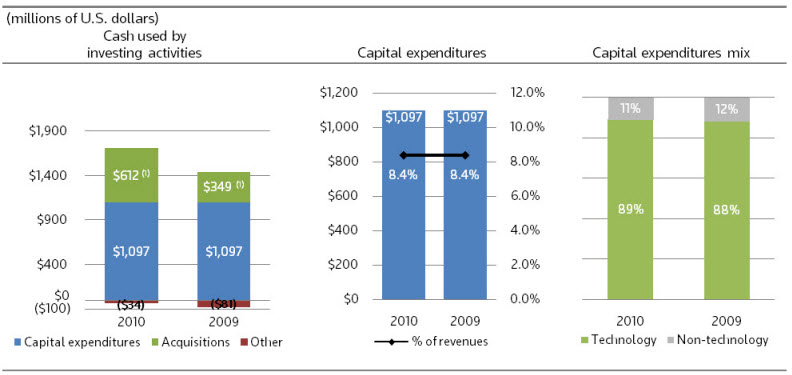

Over the last few years, we have made significant investments in our technology. Technology-related capital expenditures in 2010 represented approximately 89% of our total capital expenditures for the year. As the number of professionals around the world grows, we believe that there will be an increasing demand for our products and services. We are focused on constantly improving our technology infrastructure to meet this growing demand at an appropriate cost.

In order to provide intelligent information to business and professional customers around the world, we focus on integrating our proprietary content with technology. In particular, we use technology to maximize the value of our information. We continuously are improving our algorithms, search capabilities, user interfaces, workflow, collaboration tools, data and overall product performance in order to increase our customers’ efficiency and effectiveness.

We are continuing to develop our online delivery platforms, taking advantage of the latest technologies. Our platforms allow us to more easily combine content from our various online services, reduce product delivery costs and reduce development time for new products and services. For various global products, we use a common database platform that supports multiple applications. This allows us to deploy products quickly into numerous markets, especially where we provide country or industry-specific information that is combined with data that is used in other Thomson Reuters products.

We are also focused on further improving efficiencies to lower costs and enhance our competitive position. We are reducing the complexity and increasing the efficiency of our underlying data center infrastructure through virtualization, automation and standardization. We are also simplifying network design in our communications infrastructure.

INTELLECTUAL PROPERTY

Many of our products and services are comprised of information delivered through a variety of media, including online, software-based applications, mobile devices, books, journals, compact discs and dedicated transmission lines. Our principal IP assets include patents, trademarks, trade secrets, databases and copyrights in our content. We believe that our IP is sufficient to permit us to carry on our business as presently conducted. We also rely on confidentiality agreements to protect our rights. We continue to apply for and receive patents for our innovative technologies. Additionally, we continue to acquire patents through the acquisition of companies. We also obtain significant content and data through third party licensing arrangements with content providers. We have registered a number of website domain names in connection with our online operations.

RESEARCH AND DEVELOPMENT

Innovation is essential to our success and is one of our primary bases of competition.

We undertake significant research and development (R&D) which is then incorporated into our products, services and technology. Our R&D team includes research scientists and software developers with backgrounds in mathematics, linguistics, psychology, computer science and artificial intelligence.

We have recently filed a number of patents on topics such as system ranking, information storage, data mining, information patterns, forecasting valuation and routing trade orders. We have also published academic papers on topics such as machine learning algorithms and information retrieval.

In addition to a dedicated corporate R&D team, our business units also use innovative technology to develop products and services. Recent examples include court transcripts with synchronized video and text versions, mobile applications that deliver tailored breaking news and business information via user-selected alerting, and a significant addition to our new legal research product, WestlawNext, called foldering, which allows customers to be able to store all of their related research for future use and automatic updating. Our businesses also recently created our new Reuters Insider, Thomson Reuters Eikon and Thomson Reuters Elektron products.

SALES AND MARKETING

We primarily sell our products and services directly to our customers. In addition, we have been successful in selling some of our products and services directly to customers via the Internet. Focusing some of our marketing and sales efforts online has allowed us to broaden our range of customers and reduce sales and marketing costs.

Thomson Reuters Annual Report 2010

15

CORPORATE RESPONSIBILITY

Corporate Responsibility (CR) is an integral part of the way we do business. We have a CR policy that describes how we manage our relationships with stakeholders in four areas: the community (the places and societies in which we operate), our workplace (employees), the environment and the marketplace (customers, suppliers and investors). By articulating focus areas, we are able to define our responses to global standards and charters in ways that are meaningful and relevant to our business. Our current CR priorities are diversity, community impact, responsible sourcing and the environment. To address these priorities, we have continued to develop and implement programs and initiatives, including measurement, reporting and governance. For more information, please see the Corporate Responsibility section of our website, www.thomsonreuters.com.

COMMUNITY

In 2010, our employees exemplified a commitment to the community by volunteering nearly 16,000 hours. Through our Community Champion Awards program, we recognize and reward employee community service efforts.

The Thomson Reuters Foundation, a not-for-profit organization, leverages skills and expertise across our organization to increase trust in, and access to, the rule of law, save lives through the provision of trusted information and improve standards of journalism. In 2010, the Foundation successfully launched and continued to develop three major programs:

|

|

●

|

Emergency Information Service (EIS) provides vital information through text messages to populations affected by disaster. EIS was used in Haiti after the massive earthquake in January 2010.

|

|

|

●

|

TrustLaw is a global hub for pro bono legal services that connects lawyers with non-governmental organizations and others in need of free legal support and also provides news and information on governance.

|

|

|

●

|

AlertNet.org is a global humanitarian news website that now includes new media services. AlertNet also includes free tools and resources to help journalists cover difficult crises and multimedia reporting on underreported emergencies.

|

WORKPLACE

Our business is founded on integrity, independence and freedom from bias which is codified through the Thomson Reuters Trust Principles and complemented by our Code of Business Conduct and Ethics. All of our employees are required to acknowledge our Code of Business Conduct and Ethics, which reflects our values as a company and our approach to doing business. We also provide our employees with a confidential and anonymous helpline for reporting Code-related issues.

ENVIRONMENT

We derived 91% of our 2010 revenues from information delivered electronically, software and services. We believe that our efforts over the last decade to move more of our business from print to electronic saves vital natural resources and chemicals in printing and the shipping process. We also seek to operate our data centers and our global real estate portfolio as efficiently as possible.

In 2010, we launched a project to collect consumption data from across our business to provide a comprehensive assessment of our annual environment impact, or carbon footprint. As part of this project, we have been developing a strategy for measuring our carbon footprint across the business on a global basis.

We promote environmental best practices through our network of 75 staff-driven “Green Teams” around the world, enabling them to share ideas and promote new initiatives, such as our use of telepresence videoconferencing units in our largest locations to help reduce travel.

One additional way we address global environmental challenges is through the information we provide to customers and the public. Through Reuters Media’s dedicated environment-focused blogs and video channels, we provide news on environmental topics and encourage debate and increased awareness.

MARKETPLACE

In 2010, we launched a new supply chain ethical code that is designed to ensure that our suppliers met a specified set of standards. A number of our suppliers have agreed to comply with the code in providing services to us.

ACQUISITIONS AND DISPOSITIONS

In 2008, we completed our acquisition of Reuters for approximately $16 billion. During the last three years, we also made a number of tactical acquisitions which complemented our existing businesses. For many of these acquisitions, we purchased information or a service that we integrated into our operations to broaden the range of our offerings. These acquisitions have expanded our product offerings, enabled us to enter adjacent markets, tap new revenue streams and achieve cost efficiencies. Key tactical acquisitions in 2010 included Complinet, Point Carbon, Serengeti, Canada Law Book, Revista dos Tribunais, GeneGo and Pangea3.

Thomson Reuters Annual Report 2010

16

In addition, as part of our continuing strategy to optimize our portfolio of businesses and ensure that we are investing in parts of our business that offer the greatest opportunities to achieve growth and returns, we also actively pursued the sale of a number of businesses during the last three years. We recently decided to pursue the sale of our BARBRI business and our Scandinavian Legal and Tax & Accounting businesses from our Professional division, and we recently sold Treasura in our Markets division. For more information on acquisitions and dispositions that we made in the last three years, please see the “Management’s Discussion and Analysis” section of this annual report.

EMPLOYEES

The following table sets forth information about our employees as of December 31, 2010.

|

Thomson Reuters

|

57,900 | |||

|

Americas

|

27,900 | |||

|

Europe, Middle East and Africa

|

12,300 | |||

|

Asia

|

17,700 | |||

|

Professional division

|

26,500 | |||

|

Legal

|

15,300 | |||

|

Tax & Accounting

|

5,200 | |||

|

Healthcare & Science

|

4,600 | |||

|

Other

|

1,400 | |||

|

Markets division

|

28,800 | |||

|

Corporate headquarters

|

2,600 |

We believe that we generally have good relations with our employees, unions and work councils, although we have disputes from time to time with the various unions that represent some of our employees. Our senior management team is committed to maintaining good relations with our employees, unions and works councils.

PROPERTIES AND FACILITIES

We own and lease office space and facilities around the world to support our businesses. We believe that our properties are in good condition and are adequate and suitable for our present purposes. The following table provides summary information about our principal properties as of December 31, 2010.

|

Facility

|

Approx. sq. ft.

|

Owned/Leased

|

Principal use

|

|||

|

610 Opperman Drive,

Eagan, Minnesota

|

|

2,792,000

|

Owned

|

Legal headquarters and operating facilities

|

||

|

3 Times Square,

New York, New York

|

435,300

|

Owned/Leased2

|

Thomson Reuters headquarters and Markets division operating facilities

|

|||

|

195 Broadway,

New York, New York

|

|

435,200

|

Leased

|

Markets division and Tax & Accounting offices

|

||

|

2395 Midway Road,

Carrollton, Texas

|

|

409,150

|

Owned

|

Tax & Accounting operating facilities

|

||

|

Boston, Massachusetts1

|

358,300

|

Leased

|

Markets division operating facilities

|

|||

|

Geneva, Switzerland

|

291,160

|

Owned

|

Markets division operating facilities

|

|||

|

Canary Wharf,

London, United Kingdom

|

282,700

|

Leased

|

Markets division operating facilities

|

|||

|

RMZ Infinity, Bangalore, India

|

|

248,000

|

Leased

|

Markets division operating facilities

|

||

|

Blackwall Yard, London,

United Kingdom

|

240,000

|

Owned

|

Markets division Dockland’s Technical Center

|

|

1

|

Consists of three addresses.

|

|

2

|

We lease this facility from 3XSQ Associates, an entity owned by one of our subsidiaries and Rudin Times Square Associates LLC. 3XSQ Associates was formed to build and operate the 3 Times Square property and building in New York, New York that now serves as our corporate headquarters. 435,300 sq. ft. represents the net amount of space that we currently use under our lease. The lease covers a total of 692,200 sq. ft., of which 256,900 sq. ft. has been sub-leased.

|

Thomson Reuters Annual Report 2010

17

RISK FACTORS

The risks and uncertainties below represent the risks that our management believes are material. If any of the events or developments discussed below actually occurs, our business, financial condition or results of operations could be adversely affected. Other factors not presently known to us or that we presently believe are not material could also affect our future business and operations.

We may be adversely affected by future downturns in the markets that we serve.

Our performance depends on the financial health and strength of our customers, which in turn is dependent on the general economies in our major markets in North America, Europe and Asia. The global recession in 2009 caused disruptions and volatility in economies worldwide, particularly in the financial services industry. Although the global economy began to improve and recover in 2010, future downturns in the financial services industry in one or more of the countries in which we operate or significant trading market disruptions or suspensions could adversely affect our business. Any one or more of these events may contribute to reduced activity by our customers, decrease demand for our products and services, and adversely affect suppliers and third parties on whom we depend. The economic recession also impacted the legal industry, causing a number of law firms to increase their focus on reducing costs. In 2010, we derived approximately 85% of our revenues from financial and legal customers. Cost-cutting by any of our customer segments may also adversely affect our financial results.

We operate in highly competitive markets and may be adversely affected by this competition.

The information and news industries are highly competitive. Many of our principal competitors have substantial financial resources, recognized brands, technological expertise and market experience. Our competitors are also enhancing their products and services, developing new products and services and investing in technology to better serve the needs of their existing customers and to attract new customers. Our competitors may acquire additional businesses in key sectors that will allow them to offer a broader array of products and services. We may also face increased competition from Internet service companies and search providers that could pose a threat to some of our businesses by providing more in-depth offerings, adapting their products and services to meet the demands of their customers or combining with one of their traditional competitors to enhance their products and services. Competition may require us to reduce the price of our products and services or make additional capital investments that would adversely affect profit margins. If we are unable or unwilling to do so, we may lose market share and our financial results may be adversely affected. In addition, some of our customers have in the past and may decide again to develop independently certain products and services that they obtain from us, including through the formation of consortia. To the extent that customers become more self-sufficient, demand for our products and services may be reduced, which may adversely affect our financial results.

Increased accessibility to free or relatively inexpensive information sources may reduce demand for our products and services.

In recent years, more public sources of free or relatively inexpensive information have become available, particularly through the Internet, and this trend is expected to continue. For example, some governmental and regulatory agencies have increased the amount of information they make publicly available at no cost. In addition, several companies and organizations have made certain legal and financial information publicly available at no cost. “Open source” software that is available for free may also provide some functionality similar to that in some of our products. Public sources of free or relatively inexpensive information may reduce demand for our products and services. Although we believe our information is more valuable and enhanced through analysis, tools and applications that are embedded into customers’ workflows, our financial results may be adversely affected if our customers choose to use these public sources as a substitute for our products or services.

If we are unable to develop new products, services, applications and functionalities to meet our customers’ needs, attract new customers or expand into new geographic markets, our ability to generate revenues may be adversely affected.

Our growth strategy involves developing new products, services, applications and functionalities to meet our customers’ needs for intelligent information solutions and maintaining a strong position in the sectors that we serve. As the information and news services industries undergo rapid evolution, we must be able to anticipate and respond to our customers’ needs in order to improve our competitiveness. For example, we have made significant investments in the development and promotion of new products, such as WestlawNext, Thomson Reuters Eikon and Thomson Reuters Elektron. In addition, we plan to grow by attracting new customers and expanding into new geographic markets such as Asia, Latin America and the Middle East. It may take us a significant amount of time and expense to develop new products, services, applications and functionalities to meet needs of customers, attract new customers or expand into new geographic markets. If we are unable to do so, our ability to generate revenues may be adversely affected.

In our Professional division, our customers have increasingly been seeking products and services delivered electronically and migrating away from higher margin print and CD products.

Thomson Reuters Annual Report 2010

18

We generate a significant percentage of our revenues from recurring subscription-based arrangements, and our ability to maintain existing revenues and to generate higher revenues is dependent in part on maintaining a high renewal rate.

In 2010, 86% of our revenues were derived from subscriptions or similar contractual arrangements, which result in recurring revenues. Our revenues are supported by a relatively fixed cost base that is generally not impacted by fluctuations in revenues. Our subscription arrangements are most often for a term of one year or renew automatically under evergreen arrangements. With appropriate notice, however, certain arrangements are cancelable quarterly, particularly within our Markets division. In addition, the renewals of longer-term arrangements are often at the customer’s option. In order to maintain existing revenues and to generate higher revenues, we are dependent on a significant number of our customers to renew their arrangements with us. Our revenues could also be lower if a significant number of our customers renewed their arrangements with us, but reduced the amount of their spending.

We rely heavily on network systems and the Internet and any failures or disruptions may adversely affect our ability to serve our customers.

We are dependent on our ability to handle rapidly substantial quantities of data and transactions on computer-based networks and the capacity, reliability and security of our electronic delivery systems and the Internet. Any significant failure or interruption of these systems, including operational services, loss of service from third parties, sabotage, break-ins, war, terrorist activities, human error, natural disaster, power or coding loss and computer viruses could cause our systems to operate slowly or interrupt service for periods of time and could have a material adverse effect on our business and results of our operations. Any breach of data security caused by one of these events could also result in unintentional disclosure of, or unauthorized access to, customer data or information, which could potentially result in additional costs, lost sales, penalties and litigation. Our ability to effectively use the Internet may be impaired due to infrastructure failures, service outages at third party Internet providers or increased government regulation. In addition, we are facing significant increases in our use of power and data storage. We may experience shortage of capacity and increased costs associated with such usage. These events may affect our ability to store, handle and deliver data and services to our customers.

From time to time, update rates of market data have increased. This can sometimes impact product and network performance. Factors that have significantly increased the market data update rates include:

|

|

—

|

the emergence of proprietary data feeds from other markets;

|

|

|

—

|

high market volatility;

|

|

|

—

|

decimalization;

|

|

|

—

|

reductions in trade sizes resulting in more transactions;

|

|

|

—

|

new derivative instruments;

|

|

|

—

|

increased automatically-generated algorithmic and program trading;

|

|

|

—

|

market fragmentation resulting in an increased number of trading venues; and

|

|

|

—

|

multiple listings of options and other securities.

|

Changes in legislation and regulation pertaining to market structure and dissemination of market information may also increase update rates. While we continue to implement a number of capacity management initiatives, there can be no assurance that our company and our network providers will be able to accommodate accelerated growth of peak traffic volumes or avoid other failures or interruptions.

We are dependent on third parties for information and other services.