UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE TO

TENDER OFFER STATEMENT UNDER SECTION 14(d)(1) OR SECTION 13(e)(1)

OF THE SECURITIES EXCHANGE ACT OF 1934

AMENDMENT NO. 2

FX ALLIANCE INC.

(Name of Subject Company)

CB TRANSACTION CORP.

THOMCORP HOLDINGS INC.

THOMSON REUTERS CORPORATION

(Names of Filing Persons (Offerors))

COMMON STOCK, PAR VALUE $0.0001 PER SHARE

(Title of Class of Securities)

361202104

(CUSIP Number of Class of Securities)

Deirdre Stanley

Executive Vice President and General Counsel

Thomson Reuters Corporation

3 Times Square

New York, NY 10036

(646) 232-4000

(Name, Address and Telephone Number of Person Authorized

to Receive Notices and Communications on Behalf of Filing Persons)

Copies to:

David N. Shine, Esq.

Tiffany Pollard, Esq.

Fried, Frank, Harris, Shriver & Jacobson LLP

One New York Plaza

New York, New York 10004

Phone: (212) 859-8000

Fax: (212) 859-4000

CALCULATION OF FILING FEE

|

Transaction Valuation*

|

Amount of Filing Fee**

|

|

|

$679,000,373.00

|

$77,813.45

|

|

|

|

||

|

*

|

Estimated for purposes of calculating the filing fee only. This amount is based on the offer to purchase at a purchase price of $22.00 cash per share (i) all 28,419,880 outstanding shares of common stock, par value $0.0001 per share, of FX Alliance Inc.; (ii) all 24,061 shares of restricted common stock, par value $0.0001 per share, of FX Alliance Inc.; and (iii) 5,047,850 shares of common stock, par value $0.0001 per share, of FX Alliance Inc., issuable pursuant to outstanding options with an exercise price less than $22.00 per share, which is calculated by multiplying the number of shares underlying an outstanding option with an exercise price less than $22.00 by an amount equal to $22.00 minus the exercise price for such option, in each case as of June 30, 2012, the most recent practicable date.

|

|

**

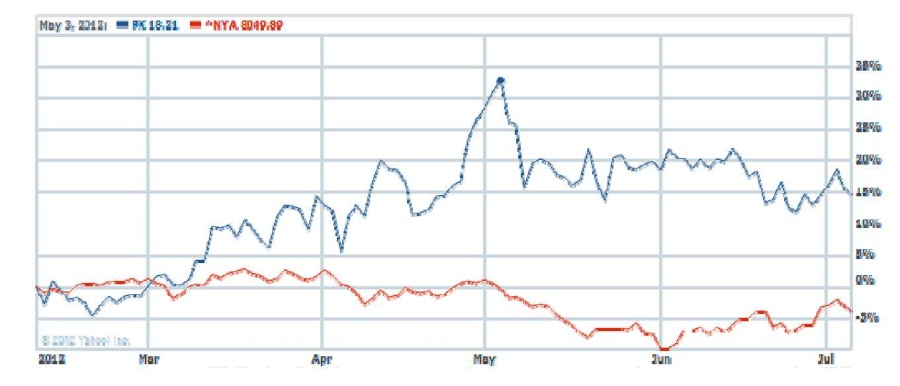

|

The amount of the filing fee is calculated in accordance with Rule 0-11 of the Securities Exchange Act of 1934, as amended, by multiplying the transaction valuation by 0.0001146.

|

|

x

|

Check box if any part of the fee is offset as provided by Rule 0-11(a)(2) and identify the filing with which the offsetting fee was previously paid. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

|

|

Amount Previously Paid:

|

$77,813.45

|

Filing Party:

|

CB Transaction Corp.,

Thomcorp Holdings Inc. and

Thomson Reuters Corporation

|

|||

|

Form or Registration No.:

|

Schedule TO

|

Date Filed:

|

July 18, 2012

|

|||

|

o

|

Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer.

|

Check the appropriate boxes below to designate any transactions to which the statement relates:

x third-party tender offer subject to Rule 14d-1.

o issuer tender offer subject to Rule 13e-4.

o going-private transaction subject to Rule 13e-3.

o amendment to Schedule 13D under Rule 13d-2.

Check the following box if the filing is a final amendment reporting the results of the tender offer. o

This Amendment No. 2 to the Tender Offer Statement on Schedule TO (this “Amendment”) filed with the U.S. Securities and Exchange Commission (the “SEC”) on July 31, 2012, amends and supplements the Tender Offer Statement on Schedule TO filed on July 18, 2012 (as amended and supplemented from time to time, the “Schedule TO”), relating to the offer by Offeror (as defined below) to purchase all of the outstanding shares of common stock, par value $0.0001 per share (each a “Share” and collectively, the “Shares”), of FX Alliance Inc., a Delaware corporation (“FX”), at a purchase price of $22.00 per Share, net to the seller in cash, without interest and less taxes required to be withheld, upon the terms and subject to the conditions set forth in the Offer to Purchase dated July 18, 2012 (the “Offer to Purchase”) and the related Letter of Transmittal (the “Letter of Transmittal”), copies of which are attached to the Schedule TO as Exhibits (a)(1)(A) and (a)(1)(B) (which, together with the Offer to Purchase, as each may be amended and supplemented from time to time, constitute the “Offer”). The Schedule TO (including the Offer to Purchase) filed with the SEC by CB Transaction Corp., a Delaware corporation (“Offeror”), Thomcorp Holdings Inc., a Delaware corporation, (“Thomcorp”) and Thomson Reuters Corporation (“Thomson Reuters”), on July 18, 2012, as amended by this Amendment No. 2 and the Solicitation/Recommendation Statement on Schedule 14D−9 filed with the SEC by FX on July 18, 2012, as amended or supplemented from time to time, contain important information about the Offer, all of which should be read carefully by FX stockholders before any decision is made with respect to the Offer. The Offer is made pursuant to the Agreement and Plan of Merger, dated as of July 8, 2012 (as it may be amended from time to time, the “Merger Agreement”), by and among Thomcorp, Offeror, FX and, solely with respect to Section 9.13 of the Merger Agreement, Thomson Reuters.

Documentation relating to the Offer has been mailed to FX stockholders and may be obtained at no charge at the website maintained by the SEC at www.sec.gov and may also be obtained at no charge by directing a request by mail to Georgeson Inc., the Information Agent for the Offer, at 199 Water Street, 26th Floor, New York, NY 10038, or by calling toll-free at (866) 277-8239.

All information set forth in the Offer to Purchase and the related Letter of Transmittal is incorporated by reference herein in response to Items 1 through 9 and Item 11 of the Schedule TO, and is supplemented by the information specifically provided in this Amendment. Capitalized terms used but not otherwise defined herein shall have the meanings ascribed to such terms in the Offer to Purchase or in the Schedule TO.

“Frequently Asked Questions” of the Offer to Purchase is hereby amended and supplemented by amending and restating the final question and answer on page 7 of the Offer to Purchase to instead read as follows:

“Do you have the financial resources to make payment?

Yes. We estimate that approximately $705 million will be needed to purchase all Shares validly tendered in the Offer to cash out certain employee stock options, to pay related fees and expenses and to complete the merger and pay the merger consideration in connection with the merger of us into FX, which is expected to follow the successful completion of the Offer (all such payments, collectively referred to as the “Necessary Payments”). Thomson Reuters, our public parent company, or one or more of its subsidiaries will provide us with sufficient funds to pay the Necessary Payments. We expect to fund the Necessary Payments with funds provided by Thomson Reuters and its subsidiaries (including Thomcorp) either through one or more capital contributions or as an intercompany loan (and the terms of any such intercompany loan have not yet been determined). Thomson Reuters and its subsidiaries will obtain such funds from cash on hand and/or cash generated from general corporate operating activities. As of June 30, 2012, Thomson Reuters and its consolidated subsidiaries had approximately $1.8 billion in cash and cash equivalents on hand. Thomson Reuters, Thomcorp and Offeror do not have any alternative financing plans or arrangements. Consummation of the Offer is not subject to any financing condition. See “Section 10 - Source and Amount of Funds.””

Item 2.

Section 8 – “Certain Information Concerning FX” of the Offer to Purchase is hereby amended and supplemented by adding the following text and tables following the sub-section captioned “FX Projections”:

“Reconciliation of Non-GAAP Financial Measures. FX’s projections include projections of FX’s “Operating Expenses,” “Adjusted EBITDA,” “Adjusted EBIT” and “Adjusted Net Income.”

“Operating Expenses” as presented by FX excludes depreciation and amortization and stock-based compensation and, for the fiscal year 2012, excludes expenses incurred in connection with FX’s initial public offering. Operating Expenses, as presented by FX, is not a financial measurement prepared in accordance with GAAP. Operating Expenses, as presented by FX, should not be considered as a substitute for operating expense prepared in accordance with GAAP. Because Operating Expenses, as presented by FX, excludes some, but not all items that affect operating expense and may vary among companies, the Operating Expenses presented by FX may not be comparable to similarly titled measures of other companies. A reconciliation of the differences between FX’s projected Operating Expenses and operating expenses, a financial measurement prepared in accordance with GAAP, is set forth below. FX did not provide us with this reconciliation in connection with our due diligence, but provided us with this reconciliation pursuant to SEC requirements in connection with this Offer to Purchase.

Reconciliation of Operating Expenses, as presented by FX, to operating expenses

|

Fiscal Year

|

Fiscal Year

|

|

|

2012

|

2013

|

|

|

($U.S. in millions)

|

||

|

Operating expenses (GAAP)

|

$84.4

|

$89.8

|

|

Less: Depreciation and amortization

|

11.9

|

14.3

|

|

Less: Stock-based compensation expense

|

4.4

|

4.8

|

|

Less: Initial public offering expenses

|

1.4

|

-

|

|

Operating Expenses (Non-GAAP)

|

$66.7

|

$70.7

|

Adjusted EBITDA is not a financial measurement prepared in accordance with GAAP. Adjusted EBITDA should not be considered as a substitute for net income or other income or cash flow data prepared in accordance with GAAP. Because Adjusted EBITDA excludes some, but not all items that affect net income and may vary among companies, the Adjusted EBITDA presented by FX may not be comparable to similarly titled measures of other companies. A reconciliation of the differences between FX’s projected Adjusted EBITDA and net income, a financial measurement prepared in accordance with GAAP, is set forth below. FX did not provide us with this reconciliation in connection with our due diligence, but provided us with this reconciliation pursuant to SEC requirements in connection with this Offer to Purchase.

Reconciliation of Adjusted EBITDA to net income

|

Fiscal Year

|

Fiscal Year

|

|

|

2012

|

2013

|

|

|

($U.S. in millions)

|

||

|

Net income (GAAP)

|

$24.7

|

$32.9

|

|

Provision for income taxes

|

16.4

|

21.8

|

|

Interest and other income (expense), net

|

(0.1)

|

-

|

|

Depreciation and amortization

|

11.9

|

14.3

|

|

Stock-based compensation expense

|

4.4

|

4.8

|

|

Initial public offering expenses

|

1.4

|

-

|

|

Adjusted EBITDA (Non-GAAP)

|

$58.7

|

$73.8

|

Adjusted EBIT is not a financial measurement prepared in accordance with GAAP. Adjusted EBIT should not be considered as a substitute for net income or other income or cash flow data prepared in accordance with GAAP. Because Adjusted EBIT excludes some, but not all items that affect net income and may vary among companies, the Adjusted EBIT presented by FX may not be comparable to similarly titled measures of other companies. A reconciliation of the differences between FX’s projected Adjusted EBIT and net income, a financial measurement prepared in accordance with GAAP, is set forth below. FX did not provide us with this reconciliation in connection with our due diligence, but provided us with this reconciliation pursuant to SEC requirements in connection with this Offer to Purchase.

Reconciliation of Adjusted EBIT to net income

|

Fiscal Year

|

Fiscal Year

|

|

|

2012

|

2013

|

|

|

($U.S. in millions)

|

||

|

Net income (GAAP)

|

$24.7

|

$32.9

|

|

Provision for income taxes

|

16.4

|

21.8

|

|

Interest and other income (expense), net

|

(0.1)

|

-

|

|

Stock-based compensation expense

|

4.4

|

4.8

|

|

Initial public offering expenses

|

1.4

|

-

|

|

Adjusted EBIT (Non-GAAP)

|

$46.8

|

$59.5

|

Adjusted Net Income is not a financial measurement prepared in accordance with GAAP. Adjusted Net Income should not be considered as a substitute for net income or other income or cash flow data prepared in accordance with GAAP. Because Adjusted Net Income excludes some, but not all items that affect net income and may vary among companies, the Adjusted Net Income presented by FX may not be comparable to similarly titled measures of other companies. A reconciliation of the differences between FX’s projected Adjusted Net Income and net income, a financial measurement prepared in accordance with GAAP, is set forth below. FX did not provide us with this reconciliation in connection with our due diligence, but provided us with this reconciliation pursuant to SEC requirements in connection with this Offer to Purchase.

Reconciliation of Adjusted Net Income to net income

|

Fiscal Year

|

Fiscal Year

|

|

|

2012

|

2013

|

|

|

($U.S. in millions)

|

||

|

Net income (GAAP)

|

$24.7

|

$32.9

|

|

Stock-based compensation expense, net of tax

|

2.7

|

2.9

|

|

Initial public offering expenses, net of tax

|

0.8

|

-

|

|

Adjusted Net Income (Non-GAAP)

|

$28.2

|

$35.8

|

Items 4 through 6, Item 8 and Item 11.

Section 13 – “The Transaction Documents” of the Offer to Purchase is hereby amended and supplemented by adding the following text to the end of the second paragraph of the sub-section captioned “The Tender and Support Agreements”:

“Copies of the Lock-Up Waivers to each of the Lock-Up Agreements with the Stockholders are filed as Exhibits (d)(6) through (d)(8) to the Schedule TO.”

Section 13 – “The Transaction Documents” of the Offer to Purchase is hereby further amended and supplemented by adding the following text to the end of the sub-section captioned “Lock-Up Waivers”:

“Copies of the Lock-Up Waivers relating to the Tender and Support Agreements are filed as Exhibits (d)(6) through (d)(8) to the Schedule TO. A copy of the lock-up waiver relating to all other stockholders subject to the letter agreements with Merrill Lynch and GS is filed as Exhibit (d)(9) to the Schedule TO.”

Item 7.

(a), (b), (d) The information set forth in Section 10 “Source and Amount of Funds” of the Offer to Purchase is hereby amended and supplemented by amending and restating it to instead read as follows:

“10. Source and Amount of Funds.

We estimate that approximately $705 million will be needed to purchase all Shares validly tendered in the Offer, to cash out certain employee stock options, to pay related fees and expenses and to complete the Merger and to pay the consideration in respect of Shares converted in the Merger into the right to receive the same per Share amount paid in the Offer (all such payments, collectively referred to as the “Necessary Payments”). Thomson Reuters, our public parent company, or one or more of its subsidiaries will provide us with sufficient funds to pay the Necessary Payments. We expect to fund the Necessary Payments with funds provided by Thomson Reuters and its subsidiaries (including Thomcorp) either through one or more capital contributions or as an intercompany loan (and the terms of any such intercompany loan have not yet been determined). Thomson Reuters and its subsidiaries will obtain such funds from cash on hand and/or cash generated from general corporate operating activities. As of June 30, 2012, Thomson Reuters and its consolidated subsidiaries had approximately $1.8 billion in cash and cash equivalents on hand. Thomson Reuters, Thomcorp and Offeror do not have any alternative financing plans or arrangements. Consummation of the Offer is not subject to any financing condition.

We do not believe that our financial condition is relevant to a decision by the holders of the Shares whether to tender Shares and accept the Offer because:

|

●

|

the Offer is being made for all outstanding Shares solely for cash, and if the holders of Shares tender their Shares, following the Merger, they will not have any continuing interest in FX, Thomson Reuters or Thomcorp; |

|

●

|

consummation of the Offer is not subject to any financing condition;

|

|

●

|

if we consummate the Offer, we expect to acquire all remaining Shares in the Merger, in cash, for the same price per share paid in the Offer; and

|

|

●

|

we, through our direct parent company, Thomcorp, our public parent company, Thomson Reuters, and other subsidiaries of Thomson Reuters, will have sufficient funds to purchase all Shares validly tendered, and not properly withdrawn, in the Offer and to provide funding for the Merger, which is expected to follow the successful completion of the Offer.”

|

Item 11.

Section 16 – “Certain Legal Matters; Regulatory Approvals” of the Offer to Purchase is hereby amended and supplemented by adding the following text at the end of the second paragraph of the sub-section captioned “U.S. Antitrust”:

“The waiting period under the HSR Act applicable to the Offer and the Merger expired effective 11:59 p.m., New York City time, on Monday, July 30, 2012. As a result, the condition of the Offer related to the expiration or termination of the waiting period under the HSR Act has been satisfied. On July 31, 2012, Thomson Reuters and FX issued a joint press release announcing the expiration of the HSR Act waiting period, a copy of which is filed as Exhibit (a)(5)(H) to the Schedule TO and is incorporated herein by reference.”

Section 16 – “Certain Legal Matters; Regulatory Approvals” of the Offer to Purchase is hereby further amended and supplemented by adding the following paragraphs to the end of the sub-section captioned “Legal Proceedings—Stockholder Litigation”:

“On July 26, 2012 stipulations of voluntary discontinuance without prejudice were filed in both Rubin v. FX Alliance Inc., et al., Index No. 652450/2012, and Dart Seasonal Products Retirement Plan v. FX Alliance Inc., et al., Index No. 652509/2012. Filed as Exhibit (a)(5)(I) to the Schedule TO is the stipulation of voluntary discontinuance filed in the Rubin litigation. Filed as Exhibit (a)(5)(J) to the Schedule TO is the stipulation of voluntary discontinuance filed in the Dart Seasonal Products Retirement Plan litigation.

On July 27, 2012, Michael Rubin commenced a putative stockholder class action lawsuit entitled Michael Rubin, on Behalf of Himself and All Others Similarly Situated v. FX Alliance Inc., et al., Case No. 7730, in the Court of Chancery of the State of Delaware. The allegations in the Delaware Court of Chancery complaint are substantially similar to the allegations contained in the amended complaint filed in Rubin v. FX Alliance Inc., et al., Index No. 652450/2012. Filed as Exhibit (a)(5)(K) to the Schedule TO is the complaint filed with the Delaware Court of Chancery.”

Item 12 of the Schedule TO is amended and supplemented by adding the following exhibits:

|

Exhibit

Number

|

Document

|

|

|

(a)(5)(H)

|

Joint Press Release, dated July 31, 2012, issued by Thomson Reuters and FX.

|

|

|

(a)(5)(I)

|

Stipulation of Voluntary Discontinuance Without Prejudice, dated July 26, 2012 (Michael Rubin, on Behalf of Himself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

|

(a)(5)(J)

|

Stipulation of Voluntary Discontinuance Without Prejudice, dated July 26, 2012 (Dart Seasonal Products Retirement Plan, on Behalf of Itself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

|

(a)(5)(K)

|

Class Action Complaint, dated July 27, 2012 (Michael Rubin, on Behalf of Himself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

|

(d)(6)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to Technology Crossover Ventures.

|

|

|

(d)(7)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to John W. Cooley.

|

|

|

(d)(8)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to Philip Z. Weisberg and Philip Z. Weisberg as trustee for the Philip Z. Weisberg 2012 Grantor Annuity Trust.

|

|

|

(d)(9)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to certain stockholders of FX.

|

[Remainder of the page is intentionally left blank]

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

|

Dated: July 31, 2012

|

CB TRANSACTION CORP.

|

|||||

|

By:

|

/s/Priscilla C. Hughes

|

|||||

|

Name:

|

Priscilla C. Hughes

|

|||||

|

Title:

|

Vice President and Secretary

|

|||||

|

Dated: July 31, 2012

|

THOMCORP HOLDINGS INC.

|

|||||

|

By:

|

/s/Priscilla C. Hughes

|

|||||

|

Name:

|

Priscilla C. Hughes

|

|||||

|

Title:

|

Vice President and Assistant Secretary

|

|||||

|

Dated: July 31, 2012

|

THOMSON REUTERS CORPORATION

|

|||||

|

By:

|

/s/Marc E. Gold

|

|||||

|

Name:

|

Marc E. Gold

|

|||||

|

Title:

|

Assistant Secretary

|

|||||

EXHIBIT INDEX

|

Exhibit

Number

|

Document

|

|

|

(a)(1)(A)

|

Offer to Purchase, dated July 18, 2012.*

|

|

|

(a)(1)(B)

|

Form of Letter of Transmittal.*

|

|

|

(a)(1)(C)

|

Form of Notice of Guaranteed Delivery.*

|

|

|

(a)(1)(D)

|

Form of Letter to Brokers, Dealers, Commercial Banks, Trust Companies and other Nominees.*

|

|

|

(a)(1)(E)

|

Form of Letter to Clients for Use by Brokers, Dealers, Banks, Trust Companies and other Nominees.*

|

|

|

(a)(1)(F)

|

Form of Summary Advertisement as published in The Wall Street Journal on July 18, 2012.*

|

|

|

(a)(5)(A)

|

Joint Press Release, dated July 9, 2012, issued by Thomson Reuters and FX (incorporated by reference to the Schedule TO-C filed by Offeror, Thomcorp and Thomson Reuters with the SEC on July 9, 2012).*

|

|

|

(a)(5)(B)

|

Press Release, dated July 18, 2012, issued by Thomson Reuters.*

|

|

| (a)(5)(C) |

Class Action Complaint dated July 13, 2012 (Rubin v. FX Alliance Inc., et al.).*

|

|

|

(a)(5)(D)

|

Press Release, dated July 24, 2012, issued by FX (incorporated by reference to Exhibit (a)(5)(D) to the Schedule 14D-9/A filed by FX with the SEC on July 24, 2012).*

|

|

|

(a)(5)(E)

|

Class Action Complaint, dated July 19, 2012 (Dart Seasonal Products Retirement Plan, individually and on behalf all others similarly situated v. FX Alliance Inc. et al.) (incorporated by reference to Exhibit (a)(5)(E) to the Schedule 14D-9/A filed by FX with the SEC on July 24, 2012).*

|

|

| (a)(5)(F) |

Amended Class Action Complaint, dated July 24, 2012 (Dart Seasonal Products Retirement Plan, individually and on behalf all others similarly situated v. FX Alliance Inc. et al.).*

|

|

|

(a)(5)(G)

|

Amended Class Action Complaint, dated July 24, 2012 (Rubin v. FX Alliance Inc., et al.).*

|

|

| (a)(5)(H) |

Joint Press Release, dated July 31, 2012, issued by Thomson Reuters and FX.

|

|

| (a)(5)(I) |

Stipulation of Voluntary Discontinuance Without Prejudice, dated July 26, 2012 (Michael Rubin, on Behalf of Himself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

| (a)(5)(J) |

Stipulation of Voluntary Discontinuance Without Prejudice, dated July 26, 2012 (Dart Seasonal Products Retirement Plan, on Behalf of Itself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

| (a)(5)(K) |

Class Action Complaint, dated July 27, 2012 (Michael Rubin, on Behalf of Himself and All Others Similarly Situated vs. FX Alliance Inc., et al.).

|

|

|

(b)(1)

|

Not applicable.

|

|

|

(d)(1)

|

Agreement and Plan of Merger, dated as of July 8, 2012, by and among Thomcorp, Offeror, Thomson Reuters (solely with respect to Section 9.13) and FX (incorporated by reference to Exhibit 2.1 to FX’s Current Report on Form 8-K, File No. 1-35423, filed with the SEC on July 11, 2012).*

|

|

|

(d)(2)

|

Tender and Support Agreement, dated as of July 8, 2012, by and among Thomcorp, Offeror, TCV VI, L.P. and TCV Member Fund, L.P.*

|

|

|

(d)(3)

|

Tender and Support Agreement, dated as of July 8, 2012, by and among Thomcorp, Offeror, and John W. Cooley.*

|

|

|

(d)(4)

|

Tender and Support Agreement, dated as of July 8, 2012, by and among Philip Z. Weisberg, in his individual capacity and in his capacity as the sole trustee of Philip Z. Weisberg 2012 Grantor Retained Annuity Trust.*

|

|

|

(d)(5)

|

Confidentiality Agreement, dated June 28, 2012, between FX and Thomson Reuters (Markets) LLC.*

|

|

|

(d)(6)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to Technology Crossover Ventures.

|

|

|

(d)(7)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to John W. Cooley.

|

|

|

(d)(8)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to Philip Z. Weisberg and Philip Z. Weisberg as trustee for the Philip Z. Weisberg 2012 Grantor Annuity Trust.

|

|

|

(d)(9)

|

Letter re: Partial Waiver of Lock-Up Agreement, dated July 26, 2012, from Merrill Lynch and GS to certain stockholders of FX.

|

|

|

(g)

|

Not applicable.

|

|

|

(h)

|

Not applicable.

|

* Previously filed.

Exhibit (a)(5)(H)

|

|

NEWS RELEASE FOR IMMEDIATE RELEASE

Thomson Reuters and FX Alliance Inc. (FXall) Announce Expiration of Hart-Scott-Rodino Act Waiting Period Relating to Tender Offer for Shares of FXall

NEW YORK, July 31, 2012 – Thomson Reuters (TSX / NYSE: TRI), the world’s leading source of intelligent information for businesses and professionals, and FXall (NYSE:FX), the leading independent global provider of electronic foreign exchange trading solutions to corporations and asset managers, today announced that the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (“HSR Act”), has expired in connection with the previously announced cash tender offer made by CB Transaction Corp., a wholly owned indirect subsidiary of Thomson Reuters, to purchase all of the outstanding shares of common stock of FXall. Expiration of the waiting period under the HSR Act satisfies one of the conditions necessary for the consummation of the tender offer.

The tender offer is scheduled to expire at midnight (Eastern Daylight Time) at the end of Tuesday, August 14, 2012, unless extended in accordance with the merger agreement and the applicable rules and regulations of the Securities and Exchange Commission (“SEC”). The closing of the tender offer remains subject to other customary terms and conditions described in the tender offer statement on Schedule TO filed with the SEC on July 18, 2012 (as amended), including the tender of at least a majority of the outstanding shares of FXall common stock on a fully diluted basis and receipt of regulatory approval from the Financial Services Authority in the United Kingdom. Following the purchase of the shares in the tender offer, FXall will become a subsidiary of Thomson Reuters.

The Depositary for the tender offer is Computershare, Inc., c/o Voluntary Corporate Actions, P.O. Box 43011, Providence, RI 02940-3011. The Information Agent for the tender offer is Georgeson Inc., 199 Water Street, 26th Floor, New York, NY 10038. The tender offer materials may be obtained at no charge by directing a request by mail to Georgeson Inc. or by calling toll-free at (866) 277-8239, and may also be obtained at no charge at the website maintained by the SEC at www.sec.gov.

Thomson Reuters

Thomson Reuters is the world's leading source of intelligent information for businesses and professionals. We combine industry expertise with innovative technology to deliver critical information to leading decision makers in the financial and risk, legal, tax and accounting, intellectual property and science and media markets, powered by the world's most trusted news organization. With headquarters in New York and major operations in London and Eagan, Minnesota, Thomson Reuters employs approximately 60,000 people and operates in over 100 countries. Thomson Reuters shares are listed on the Toronto and New York Stock Exchanges. For more information, go to www.thomsonreuters.com.

FXall

FXall is the leading independent global provider of electronic foreign exchange trading solutions, with over 1,000 institutional clients worldwide. FXall’s offices in New York, Boston, Washington, London, Zurich, Hong Kong, Tokyo, Singapore, Sydney and Mumbai serve the needs of active traders, asset managers, corporate treasurers, banks, broker-dealers and prime brokers. For more information on FXall, visit www.fxall.com.

Important Information

This press release is for informational purposes only and is not an offer to buy or the solicitation of an offer to sell any of the FXall common shares. The offer to buy the outstanding shares of common stock of FXall is being made pursuant to a tender offer statement on Schedule TO containing an offer to purchase, form of letter of transmittal and related materials filed by CB Transaction Corp. with the Securities and Exchange Commission on July 18, 2012. FXall has filed a solicitation/recommendation statement on Schedule 14D-9 with respect to the tender offer with the Securities and Exchange Commission. The tender offer statement (including the offer to purchase, related letter of transmittal and other tender offer documents) and the solicitation/recommendation statement, as they may be amended from time to time, contain important information that should be read carefully before making any decision to tender securities in the tender offer. These materials have been or will be sent free of charge to all stockholders of FXall. Shareholders may also obtain a free copy of these materials (and all other tender offer documents filed with the Securities and Exchange Commission) on the Securities and Exchange Commission's website at www.sec.gov. The Schedule TO (including the offer to purchase and related materials) and the Schedule 14D-9 (including the solicitation/recommendation statement), may also be obtained for free by contacting Georgeson Inc., the information agent for the tender offer, toll-free at (866) 277-8239.

Thomson Reuters Cautionary Note Regarding Forward Looking Statements

Certain statements in this press release are forward looking. Such statements may include, but are not limited to, statements about the benefits of combining Thomson Reuters and FXall’s electronic foreign exchange trading activities including future financial and operating results, the timing for the closing of the acquisition, satisfaction of the conditions necessary for the consummation of the tender offer, the combined company’s plans, objectives, expectations and intentions and other statements that are not historical facts. There can be no assurance that the acquisition of FXall will be completed. These forward-looking statements are based on certain assumptions and reflect current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Some of the factors that could cause actual results to differ materially from current expectations are discussed in materials that Thomson Reuters from time to time files with, or furnishes to, the Canadian securities regulatory authorities and the SEC. Thomson Reuters annual and quarterly reports are also available in the “Investor Relations” section of www.thomsonreuters.com. There is no assurance that any forward-looking statements will materialize. You are cautioned not to place undue reliance on forward-looking statements, which reflect expectations only as of the date of this filing.

FXall Cautionary Note Regarding Forward-Looking Statements

Certain statements in this press release constitute forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of FXall to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Any statements that refer to expectations or other characterizations of future events, circumstances or results, including, without limitation, all statements related to the proposed business combination transaction and related transactions and the outlook for FXall’s businesses, performance and opportunities and regulatory approvals, the anticipated timing of filings and approvals relating to the transaction; the expected timing of the completion of the transaction; the ability to complete the transaction considering the various closing conditions; and any assumptions underlying any of the foregoing. Investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and are cautioned not to place undue reliance on these forward-looking statements. Actual results may differ materially from those currently anticipated due to a number of risks and uncertainties, including uncertainties as to the timing of the tender offer and business combination; uncertainties as to how many of FXall’s stockholders will tender their stock in the offer; the possibility that competing offers will be made; the possibility that various closing conditions for the transaction may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant approval for the consummation of the transaction; the effects of disruption from the transaction making it more difficult to maintain relationships with employees, customers, other business partners or governmental entities; other business effects, including the effects of industry, economic or political conditions outside of FXall’s control; transaction costs; actual or contingent liabilities; and other risks and uncertainties discussed in documents filed with the SEC by FXall from time to time, as well as the tender offer documents filed by Thomson Reuters and the solicitation/recommendation statement filed by FXall. Investors and security holders are able to obtain free copies of the documents filed with the SEC by FXall on the Investor Relations section of FXall website at www.fxall.com. FXall does not undertake any obligation to update any forward-looking statements as a result of new information, future developments or otherwise, except as expressly required by law.

CONTACTS

THOMSON REUTERS

|

Alan Duerden

PR Director, Thomson Reuters

D: +44 20 7542 0561

alan.duerden@thomsonreuters.com

|

Frank J. Golden

Senior Vice President,

Investor Relations

D:+1 646 2235288

frank.golden@thomsonreuters.com

|

|

|

|

|

FXALL

|

|

|

Dafina Grapci-Penney

D: +44 20 7324 5484

M: +44 7525335733

dafina.grapci-penney@greentarget.co.uk

|

Andrew Posen

Head of Investor Relations, FXall

D: +1 646 268 9952

andrew.posen@fxall.com

|

● thomsonreuters.com

Exhibit (a)(5)(I)

|

SUPREME COURT OF THE STATE OF NEW YORK

COUNTY OF NEW YORK

|

||

|

x

|

||

|

:

|

||

|

MICHAEL RUBIN, on Behalf of Himself and All

|

:

|

Index No. 652450/2012

|

|

Others Similarly Situated,

|

:

|

|

|

:

|

||

|

:

|

||

|

Plaintiff,

|

:

|

|

|

:

|

STIPULATION OF VOLUNTARY

|

|

|

vs.

|

:

|

DISCONTINUANCE WITHOUT |

|

:

|

PREJUDICE PURSUANT TO | |

|

FX ALLIANCE INC., PHILIP Z. WEISBERG,

|

:

|

C.P.L.R. 3217(a)(2) and (c) |

|

KATHLEEN CASEY, CAROLYN CHRISTIE,

|

:

|

|

|

JAMES L. FOX, GERALD D. PUTNAM, JR.,

|

:

|

|

|

JOHN C. ROSENBERG, PETER TOMOZAWA,

|

:

|

|

|

ROBERT TRUDEAU, THOMSON REUTERS

|

:

|

|

|

CORPORATION, THOMCORP HOLDINGS

|

:

|

|

| INC., and CB TRANSACTION CORP., |

:

|

|

| : | ||

|

Defendants.

|

:

|

|

|

:

|

||

|

x

|

WHEREAS, Plaintiff filed this action on July 13, 2012 asserting claims in connection with a merger transaction involving FX Alliance, Inc., and Thomson Reuters Corporation (the "FXall Merger");

WHEREAS a substantially similar action was filed in the Supreme Court New York County captioned Dart Seasonal Products Retirement Plan v. FX Alliance Inc., et al., Index No. 652509/2012 on July 19, 2012;

WHEREAS, no party is an infant or incompetent person for whom a committee has been appointed and no person not a served party has an interest in the subject matter of the action;

IT IS HEREBY STIPULATED AND AGREED, by and between the undersigned counsel, that:

1. Pursuant to C.P.L.R. 3217(a)(2) and (c), the above-captioned action is hereby, discontinued and dismissed without prejudice and without costs or attorneys' fees to either party as against the other.

2. This stipulation may be filed electronically without further notice with the Clerk of the Court.

SUBMITTED BY:

|

WEISS & LURIE

|

||||

|

By:

|

/s/ Joseph H. Weiss

|

|||

|

Joseph H. Weiss

Richard A. Acocelli

1500 Broadway, 16th Floor

New York, New York 10036

Telephone: 212/682-3025

212/682-3010 (fax)

|

||||

|

Attorneys for Plaintiff Michael Rubin

|

||||

|

KIRKLAND & ELLIS LLP

|

FRIED, FRANK, HARRIS, SHRIVER &

JACOBSON LLP

|

|||

|

By:

|

/s/ Adam T. Humann

|

By:

|

/s/ Justin Santolli

|

|

|

Yosef J. Riemer

Adam T. Humann

Shireen A. Barday

601 Lexington Avenue

New York, NY 10022

Telephone: 212/446-4800

212/446-4900 (fax)

|

David B. Hennes

Justin Santolli

One New York Plaza

New York, New York 10004

Telephone: 212/859-8000

212/859-4000 (fax)

|

|||

|

Attorneys for Defendants FX

Alliance, Inc. and Philip Z. Weisberg

|

Attorneys for Defendants Thomson Reuters

Corporation, Thomcorp Holdings Inc., and

CB Transaction Corp.

|

Exhibit (a)(5)(J)

|

SUPREME COURT OF THE STATE OF NEW YORK

COUNTY OF NEW YORK

|

||

|

x

|

||

|

:

|

||

|

DART SEASONAL PRODUCTS RETIREMENT

|

:

|

Index No. 652509/2012

|

|

PLAN, on Behalf of Itself and All Others Similarly

|

:

|

|

|

Situated,

|

:

|

|

|

:

|

||

|

Plaintiff,

|

:

|

STIPULATION OF VOLUNTARY

|

|

:

|

DISCONTINUANCE WITHOUT | |

|

vs.

|

:

|

PREJUDICE PURSUANT TO |

|

:

|

C.P.L.R. 3217(a)(2) and (c) | |

|

FX ALLIANCE INC., PHILIP Z. WEISBERG,

|

:

|

|

|

KATHLEEN CASEY, CAROLYN CHRISTIE,

|

:

|

|

|

JAMES L. FOX, GERALD D. PUTNAM, JR.,

|

:

|

|

|

JOHN C. ROSENBERG, PETER TOMOZAWA,

|

:

|

|

|

ROBERT TRUDEAU, and THOMSON REUTERS

|

:

|

|

|

CORPORATION,

|

:

|

|

|

:

|

||

|

Defendants.

|

:

|

|

|

:

|

||

|

x

|

WHEREAS, Plaintiff filed this action on July 19, 2012 asserting claims in connection with a merger transaction involving FX Alliance, Inc., and Thoinson Reuters Corporation (the "FXall Merger");

WHEREAS a substantially similar action was filed in the Supreme Court New York County captioned Michael Rubin v. FX Alliance Inc., et al., Index No. 652450/2012 on July 13, 2012;

WHEREAS, no party is an infant or incompetent person for whom a committee has been appointed and no person not a served party has an interest in the subject matter of the action;

IT IS HEREBY STIPULATED AND AGREED, by and between the undersigned counsel, that:

1. Pursuant to C.P.L.R. 3217(a)(2) and (c), the above-captioned action is hereby, discontinued and dismissed without prejudice and without costs or attorneys' fees to either party as against the other.

2. This stiplulation may be filed electronically without further notice with the Clerk of the Court.

SUBMITTED BY:

|

ROBBINS GELLER RUDMAN &

DOWD LLP

|

||||

|

By:

|

/s/ Mark S. Reich

|

|||

|

Samuel H. Rudman

Mark S. Reich

Andrea Y. Lee

58 South Service Rd., Ste 200

Melville, NY 11747

Telephone: 613/367-7100

631/367-1173 (fax)

|

||||

|

Attorneys for Plaintiff Dart Seasonal

Products Retirement Plan

|

||||

|

KIRKLAND & ELLIS LLP

|

FRIED, FRANK, HARRIS, SHRIVER &

JACOBSON LLP

|

|||

|

By:

|

/s/ Adam T. Humann

|

By:

|

/s/ Justin Santolli

|

|

|

Yosef J. Riemer

Adam T. Humann

Shireen A. Barday

601 Lexington Avenue

New York, NY 10022

Telephone: 212/446-4800

212/446-4900 (fax)

|

David B. Hennes

Justin Santolli

One New York Plaza

New York, New York 10004

Telephone: 212/859-8000

212/859-4000 (fax)

|

|||

|

Attorneys for Defendants FX

Alliance, Inc. and Philip Z. Weisberg

|

Attorneys for Defendants Thomson Reuters

Corporation

|

Exhibit (a)(5)(K)

|

IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE

|

||

|

x

|

||

|

:

|

||

|

MICHAEL RUBIN, on Behalf of Himself and

|

:

|

|

|

All Others Similarly Situated,

|

:

|

|

|

:

|

||

|

:

|

||

|

Plaintiff,

|

:

|

|

|

:

|

|

|

|

vs.

|

:

|

C.A. No. |

|

:

|

||

|

FX ALLIANCE INC., PHILIP Z.

|

:

|

|

|

WEISBERG, KATHLEEN CASEY,

|

:

|

|

|

CAROLYN CHRISTIE, JAMES L. FOX,

|

:

|

|

|

GERALD D. PUTNAM, JR., JOHN C.

|

:

|

|

| ROSENBERG, PETER TOMOZAWA, | : | |

|

ROBERT TRUDEAU, THOMSON

|

:

|

|

|

REUTERS CORPORATION, THOMCORP

|

:

|

|

| HOLDINGS INC., and CB TRANSACTION |

:

|

|

| CORP., | : | |

| : | ||

|

Defendants.

|

:

|

|

|

:

|

||

|

x

|

CLASS ACTION COMPLAINT

Michael Rubin (“Plaintiff”) respectfully submits this class action complaint by and through his undersigned counsel and makes the following allegations predicated upon the investigation undertaken by Plaintiff’s counsel:

NATURE OF THE ACTION

1. This is a shareholder class action brought by Plaintiff on behalf of himself and all other similarly situated public shareholders of FX Alliance Inc. (“FX” or the “Company”) to enjoin the proposed buyout through an all-cash tender offer (the “Proposed Transaction”) of the publicly owned shares of FX’s common stock by Thomcorp Holdings Inc. (“Thomcorp”) through its wholly owned subsidiary CB Transaction Corp. (“CB” or “Merger Sub”), and their parent, Thomson Reuters Corporation (“Thomson Reuters”). In pursuing the Proposed Transaction, each of the Defendants (defined infra) violated applicable law by directly breaching and/or aiding breaches of fiduciary duties owed to Plaintiff and the other public shareholders of FX.

2. On July 9, 2012, FX and Thomson Reuters jointly announced that they had entered into an Agreement and Plan of Merger the previous day (the “Merger Agreement”) pursuant to which Thomson Reuters, through its wholly-owned subsidiaries, will acquire FX in the Proposed Transaction for $22 cash per share (the “Merger Consideration”), for a total consideration of approximately $616 million.

3. The Proposed Transaction is the product of a flawed process designed to ensure the sale of FX to Thomson Reuters on terms preferential to Thomson Reuters, but detrimental to Plaintiff and the other public shareholders of FX.

4. Thomson Reuters and FX’s directors (the Individual Defendants herein) agreed to enter into the Merger Agreement through a sham negotiation process. The Individual Defendants failed to conduct a legitimate auction or perform a real market check. What is more, the Individual Defendants then agreed to an array of buyer-friendly terms in the Merger Agreement designed to fend off any other competing bidders. These preclusive measures are critical because all of the Defendants know that FX is a leader in its field – so much so that the merging of FX’s foreign exchange platform with Thomson Reuters’ will create the largest electronic trading pool in foreign exchange trading. In one fell swoop, Thomson Reuters is eliminating a strong competitor and taking its business prospects for itself.

5. More specifically, Thomson Reuters had an intense strategic interest in FX that predated the Company’s February 8, 2012 initial public offering (“IPO”). Thomson Reuters first approached FX to discuss the potential for a “joint marketing arrangement” with the Company in December of 2011, which shortly thereafter led to a non-disclosure agreement between the two companies, exchange of non-public information, and multiple high-level discussions. Instead of consummating a joint marketing arrangement, however, Thomson Reuters made an all-cash offer to purchase FX on May 18, 2012. Weeks of private negotiations between the two companies ensued, but it was not until a month later, on June 18 and 19, that J.P. Morgan contacted eight other parties to “solicit their interest in pursuing a possible transaction with the Company.”

6. Unsurprisingly, the Company was unable to secure a firm offer from any of the other parties. It is evident that market was aware of the Company’s engagement with Thomson Reuters in some fashion since at least the end of 2011 and that the other parties viewed the Thomson Reuters transaction with the Company as a fait accompli. The “auction process” was not undertaken in good faith and was, in essence, a single-bidder process with no subsequent market check. As a result, the Proposed Transaction undervalues FX shares and their value to FX shareholders. Indeed, FX shareholders and the market generally have indicated their skepticism with the price associated with the Proposed Transaction by bidding the market price of FX shares as high as $22.50 per share after the Proposed Transaction was announced on July 9, 2012.

7. Moreover, the deal is virtually locked up and certain to close without further shareholder approval because Thomson Reuters demanded a concurrent tender and support agreement (“Support Agreement”) whereby Chairman and Chief Executive Officer (“CEO”) Philip Z. Weisberg (“Weisberg”), Chief Financial Officer (“CFO”) John W. Cooley (“Cooley”) and FX’s largest shareholder, Technology Crossover Ventures (through its TCV VI and TCV Member Fund) (“TCV”) have agreed to tender to Thomson Reuters the 9,252,943 FX shares they own or control, which represents approximately 32.5% of outstanding shares. In addition, the Company has also granted Thomson Reuters a “Top Up Option,” which in turn would allow Thomson Reuters to complete the transaction via a short form merger without shareholder approval, as more fully described infra. Thus, although ostensibly at least a majority of FX’s 28,474,998 outstanding shares must be tendered in order to trigger the Top Up Option, the reality is Defendants require less than 5,000,000 of the remaining outstanding shares (which equals 18% of the total outstanding shares and a little more than 25% of the outstanding public shares not subject to the Support Agreement) to tender in order to consummate the merger without shareholder approval.

8. The shortcomings in the sales process are further compounded by the July 18, 2012 solicitation/recommendation statement filed by FX on Schedule 14D-9 (the “14D-9”) with the United States Securities and Exchange Commission (“SEC”), which is deficient and fails to provide FX’s shareholders with adequate information to decide whether to elect to tender their shares into the Proposed Transaction. The 14D-9 omits and/or misrepresents material information concerning, among other things: (a) the sales process for the Company; (b) the data and inputs underlying the financial valuation exercises that purport to support the so-called fairness opinion (“Fairness Opinion”) provided by the Company’s financial advisor, J.P. Morgan Securities LLC (“J.P. Morgan”); and (c) details concerning J.P. Morgan’s potential conflict of interest.

9. For example, the disclosures regarding the financial projections for FX, which are among the most important disclosures to shareholders faced with a decision whether to divest ownership of their Company, are inadequate and appear to be misleading. Critically, the 14D-9 fails to adequately disclose in a useful and meaningful way the financial projections provided to the FX Board of Directors (the “Board”) by management on May 29 and used by its financial advisor, J.P. Morgan. While the 14D-9 includes management projections that (without elaboration) describe three “cases” in which FX continues as a stand-alone company, the 14D-9 does not provide or disclose projections based upon a potential “joint marketing agreement” with Thomson Reuters that would provide shareholders the basis for determining whether it was in the best interest of shareholders to remain a stand-alone and partnering with Thomson Reuters. This is critical since, as discussed above, the primary strategic alternative for the two companies prior to the merger was the “joint marketing” process that led to Thomson Reuters’ May 18 initial bid of $19.50 and multiple meetings and telephone calls between May 23 and 29, during which the main topic was the “complementary aspects” of the companies’ businesses (including expanding global distribution network in emerging markets). During this time management prepared the projections and presented them to the Board on May 29. It is obvious that assumptions regarding FX’s potential going forward as a stand-alone with a marketing agreement in place with Thomson Reuters should have been included in projections, should have been considered by management and the Board, and should be disclosed to shareholders so they can decide whether they would be better off reaping the benefit of the joint marketing arrangement rather than being shut out and Thomson Reuters reaping the benefit solely for itself.

10. The 14D-9 should have been drafted to fulfill the purpose for which it is intended: to provide FX’s shareholders with the material information they need to make an informed decision on the Proposed Transaction. Instead, the 14D-9 appears to have been drafted solely with an eye towards defending the unfair cash out agreed to through the sham negotiation process.

11. For these reasons and the reasons set forth in more detail herein, Plaintiff seeks to enjoin Defendants from consummating the Proposed Transaction or, in the event the Proposed Transaction is consummated, recover damages resulting from the Individual Defendants’ violations of their fiduciary duties of good faith, due care, and full and fair disclosure.

12. Only through the exercise of this Court’s equitable powers can Plaintiff and the Class (as defined below) be fully protected from the immediate and irreparable injury which Defendants’ actions threaten to inflict.

THE PARTIES

13. Plaintiff, Michael Rubin, is, and has been at all relevant times hereto, a holder of FX common stock.

14. Defendant FX is a Delaware corporation with its executive offices located at 909 Third Avenue, Third Floor, New York, New York 10022. FX is an independent global provider of electronic foreign exchange trading solutions. The Company touts itself as being the global leader of its industry with over 1,000 institutional clients worldwide, serving the needs of active traders, asset managers, corporate treasurers, banks, broker-dealers and prime brokers. The Company’s stock trades on the New York Stock Exchange under the ticker symbol “FX.”

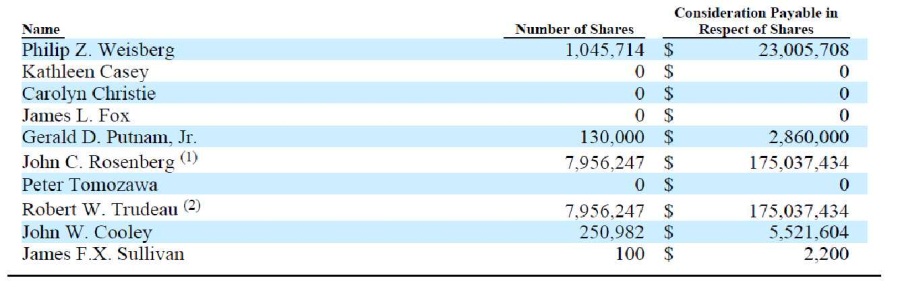

15. Defendant Weisberg has served as Chairman and CEO of FX since its inception in 2000. Holding approximately 1.04 million FX shares and 1.14 million unexercised options, he is expected to net $35 million upon the consummation of the Proposed Transaction.

16. Defendant Kathleen Casey (“Casey”) has served as an FX director since March 2012. She is Chair of the Corporate Governance and Nominating Committee, and a member of the Audit Committee.

17. Defendant Caroline Christie (“Christie”) has served as an FX director since March 2012 and is a member of the Audit Committee.

18. Defendant James L. Fox (“Fox”) has served as an FX director since March 2012 and is Chair of the Audit Committee.

19. Defendant Gerald D. Putnam, Jr. (“Putnam”) has served as an independent FX director since July 2008 and is a member of both the Compensation Committee and the Corporate Governance and Nominating Committee.

20. Defendant John C. Rosenberg (“Rosenberg”) has served as an FX director since October 2009 and is a member of the Board’s Audit Committee. Rosenberg is also a general partner with TCV, the Company’s largest shareholder.

21. Defendant Peter Tomozawa (“Tomozawa”) has served as an FX director since March 2012 and is a member of both the Compensation Committee and the Corporate Governance and Nominating Committee.

22. Defendant Robert Trudeau (“Trudeau”) has served as an FX director since August 2006 and chairs the Board’s Compensation Committee. Trudeau is also a general partner with TCV, the Company’s largest shareholder.

23. Defendant Thomson Reuters maintains its principal place of business at 3 Times Square, New York, New York 10036. Thomson Reuters is an international news agency and information delivery business. Thomson Reuters trades on both the New York Stock Exchange and the Toronto Stock Exchange under the ticker symbol “TRI.”

24. Defendant Thomcorp is a Delaware corporation and a subsidiary of Thomson Reuters and is the actual party to the Merger Agreement with FX dated July 8, 2012.

25. Defendant CB is a Delaware corporation and a wholly-owned subsidiary of Thomcorp formed for the sole purpose of effectuating the Proposed Transaction. All references herein to Defendant Thomson Reuters include Defendants Thomcorp and Merger Sub.

26. The Defendants listed in paragraphs 15 through 22 are collectively referred to herein as the “Board” or “Individual Defendants.”

27. Each Individual Defendant owed and owes FX and its public shareholders fiduciary obligations and were and are required to: use their ability to control and manage FX in a fair, just, and equitable manner; act in furtherance of the best interests of FX and its public shareholders, including, but not limited to, obtaining a fair and adequate price for FX’s shares; refrain from abusing their positions of control; disseminate complete and accurate information material to a shareholder’s decision whether to approve the Proposed Transaction; and not to favor their own interests at the expense of public shareholders.

FIDUCIARY DUTIES OF THE INDIVIDUAL DEFENDANTS

28. By reason of their positions as officers and/or directors of the Company and because of their ability to control the business and corporate affairs of the Company, the Individual Defendants owe the Company and its shareholders the fiduciary obligations of good faith, trust, loyalty, candor, and due care, and were and are required to use their utmost ability to control and manage the Company in a fair, just, honest, and equitable manner. The Individual Defendants were and are required to act in furtherance of the best interests of the Company and its shareholders so as to benefit all shareholders equally and not in furtherance of their personal interest or benefit.

29. Each director and officer of the Company owes to the Company and its shareholders the fiduciary duty to exercise good faith and diligence in the administration of the affairs of the Company and in the use and preservation of its property and assets, and the highest obligations of fair dealing.

30. The Individual Defendants, because of their positions of control and authority as directors and/or officers of the Company, were able to and did, directly and/or indirectly, exercise control over the wrongful acts complained of herein.

31. At all times relevant hereto, each of the Individual Defendants was the agent of each of the other Individual Defendants and of FX, and was at all times acting within the course and scope of such agency.

32. To discharge their duties, the officers and directors of the Company were required to exercise reasonable and prudent supervision over the management, policies, practices and controls of the Company. By virtue of such duties, the officers and directors of the Company were required to, among other things:

(a) exercise good faith in ensuring that the affairs of the Company were conducted in an efficient, business-like manner so as to make it possible for the Company to provide the highest level of performance;

(b) exercise good faith in ensuring that the Company was operated in a diligent, honest and prudent manner and complied with all applicable federal and state laws, rules, regulations and requirements, including acting only within the scope of its legal authority;

(c) when placed on notice of illegal or imprudent conduct committed by the Company or its employees, exercise good faith in taking appropriate measures to prevent and correct such conduct; and

(d) exercise good faith in supervising the preparation, filing and/or dissemination of financial statements, press releases, audits, reports or other information required by law, and in examining and evaluating any reports or examinations, audits, or other financial information concerning the financial condition of the Company.

CLASS ACTION ALLEGATIONS

33. Plaintiff brings this action pursuant to Court of Chancery Rule 23, individually and on behalf of the holders of the common stock of the Company, who have been and/or will be harmed as a result of the wrongful conduct alleged herein (the “Class”). Excluded from the Class are Defendants herein and any person, firm, trust, corporation, or other entity related to or affiliated with any of the Defendants.

34. This action is properly maintainable as a class action for the following reasons:

(a) The Class is so numerous that joinder of all members is impracticable. According to the Company’s filings with the SEC, as of July 12, 2012, there were 28,474,998 shares of FX common stock validly issued and outstanding, held by hundreds, if not thousands, of record and beneficial shareholders. The actual number of public shareholders of FX will be ascertained through discovery.

(b) Plaintiff is committed to prosecuting this action and has retained competent counsel experienced in litigation of this nature. Plaintiff’s claims are typical of the claims of the other members of the Class and Plaintiff has the same interests as the other members of the Class. Plaintiff is an adequate representatives of the Class and will fairly and adequately protect the interests of the Class.

(c) The prosecution of separate actions by individual members of the Class would create the risk of inconsistent or varying adjudications with respect to individual members of the Class, which would establish incompatible standards of conduct for Defendants, or adjudications with respect to individual members of the Class that would, as a practical matter, be dispositive of the interests of the other members not parties to the adjudications or substantially impede their ability to protect their interests.

(d) To the extent Defendants take further steps to effectuate the Proposed Transaction, preliminary and final injunctive relief on behalf of the Class as a whole will be entirely appropriate because Defendants have acted, or refused to act, on grounds generally applicable and causing injury to the Class.

35. There are questions of law and fact which are common to the Class and which predominate over questions affecting any individual Class member. The common questions include, inter alia, the following:

(a) Whether Defendants have engaged in and are continuing to engage in conduct which unfairly benefits Defendants at the expense of the members of the Class;

(b) Whether the Individual Defendants, as officers and/or directors of the Company, are violating their fiduciary duties to Plaintiff and the other members of the Class;

(c) Whether Plaintiff and the other members of the Class would be irreparably damaged were Defendants not enjoined from the conduct described herein;

(d) Whether the Individual Defendants have breached and continue to breach their fiduciary duties of loyalty, care, good faith, and candor to FX’s shareholders; and

(e) Whether FX and Thomson Reuters have aided and abetted the Individual Defendants’ breaches of fiduciary duties.

SUBSTANTIVE ALLEGATIONS

Background of the Company

36. FX is the leading independent global provider of electronic foreign exchange trading solutions, with over 1,000 institutional clients worldwide. With its proprietary technology platform, the Company provides institutional clients with 24-hour direct access, five days per week, to the foreign exchange market and delivers efficient and reliable foreign price discovery, trade execution, and automation of pre-trade and post-trade transaction workflow for more than 400 currency pairs with access to liquidity from the world’s leading banks and other liquidity providers.

37. In 2011, the Company was named, among other things, “Best Online Foreign Exchange Trading System” in Global Finance Best Foreign Exchange Providers, “Best Professional Electronic Trading Venue” in FX Week Best Banks Awards, “Best Foreign Exchange Trading Platform” in Financial News Awards Europe 2011, and “Best Trading Platform for Asset Managers” in 2011 in Profit & Loss Digital Market Awards. Thus far in 2012, the Company has been named, among other things, “Best Platform for Asset Managers” at the Profit & Loss Readers’ Choice Digital Markets Awards, “Best Independent Multibank Platform” for the eleventh consecutive year in Euromoney FX Poll.

38. FX became a publicly traded company recently, on February 8, 2012, when it completed its IPO of 5,980,000 shares of common stock, at the offered price of $12.00 per share. All of the shares were sold in the IPO. However, unlike most IPOs, the Company did not receive any proceeds from the sale of shares by the selling shareholders.

39. Since its IPO, the Company has continued to expand its business, with great promise. For example, FX just announced on July 2, 2012 that it launched a multibank options trading platform by which the Company’s clients can, in a single platform, trade spot, forwards, swaps, non-deliverable forwards, precious metals and money markets, as well as price and trade options.

Background to the Proposed Transaction

40. According to the 14D-9, the first steps that led to the Proposed Transaction occurred in December 2011 when Andrew Hausman, Managing Director, Fixed Income & Foreign Exchange of Thomson Reuters, contacted James Kwiatkowski, Global Head of Sales of the Company, to discuss the potential for a joint marketing arrangement between Thomson Reuters and the Company.

41. These talks eventually turned serious enough for Thomson Reuters and the Company to enter into a mutual non-disclosure agreement with respect to such a joint marketing arrangement in January 2012.

42. Between January and May of 2012 (which included the time during which FX was preparing for its IPO), the Company and Thomson Reuters held various meetings and discussions relating to the potential for a joint marketing arrangement, and at the same time, exchanged non-public information. In essence, Thomson Reuters had the benefit of a five month long due diligence process on the Company.

43. On or about May 18, 2012 a meeting was held at the Company’s principal office in New York ostensibly to discuss “the potential for a joint marketing arrangement and other strategic matters.” The meeting was attended by various executives of Thomson Reuters, Defendants Weisberg and Trudeau, and John W. Cooley, the Company’s Chief Financial Officer (“CFO”), on behalf of the Company. At the meeting, representatives of Thomson Reuters indicated verbally that Thomson Reuters would be prepared to make an all-cash offer for 100% of the outstanding shares of the Company at a price of $19.50 per share. Weisberg responded by noting that the Company had recently undergone an IPO and informed the representatives of Thomson Reuters that the Company was not prepared to engage in a sale process, but that he would discuss the Thomson Reuters proposal with the Company Board.

44. The following day J.P. Morgan was chosen as the Company’s financial advisor with respect to Thomson Reuters’ proposal.

45. On May 21, 2012, a full meeting of the Board was held along with executive officers of the Company at which the Board rejected Thomson Reuters’ proposal and authorized the Company’s management to prepare projections for the Company. Significantly, none of the projections disclosed in the 14D-9 take into account the assumption of the potential for a joint marketing arrangement with Thomson Reuters.

46. Between May 23, 2012 and June 8, 2012 there were various meeting and discussions between the Company, its advisors, and Thomson Reuters and its advisors, until on June 8, 2012 Thomson Reuters stated its “best and final” offer of $22.00 per share.

47. It was not until June 13, 2012, after the Company had in essence, if not actually, accepted Thomson Reuters’ offer, that the Board established a Transaction Committee to oversee the “situation.” Subsequently, it was not until June 18 and 19 that the Company’s financial advisor contacted eight other parties to “solicit their interest in pursuing a possible transaction with the Company.” Between that time and the announcement of the Proposed Transaction on July 9, 2012, there were indications of interest from other parties even in the “low 20s.” However, the Company was not able to obtain a firm offer from any of the other parties. It is evident that the market was aware of the Company’s engagement with Thomson Reuters in some fashion since at least the end of 2011 and that the other parties viewed the Thomson Reuters transaction with the Company as a done deal. The “auction process” was not undertaken in good faith and this was, in essence, a single-bidder process with no subsequent market check.

The Proposed Transaction

48. On July 9, 2012, FX announced that it had entered into the Merger Agreement with Thomson Reuters whereby the latter will acquire 100% of the Company’s outstanding stock for $22.00 per share in cash. The Proposed Transaction is expected to close in the third quarter of 2012.

49. Under the terms of the Merger Agreement, Thomson Reuters will launch a tender offer for the Proposed Transaction, subject to regulatory approval. Pursuant to the Merger Agreement, Thomson Reuters did, in fact, launch a tender offer on July 18, 2012, a scant ten days after the proposed acquisition was announced. The tender offer will expire on August 14, 2012, only 20 business days after the tender offer was commenced. The Board recommends that all FX shareholders tender their shares in favor of the Proposed Transaction. Shares not tendered will be converted into the right to receive cash equal to the Merger Consideration.

50. Moreover, the Company’s largest shareholder, TCV, along with Defendant Weisberg and FX’s CFO Cooley, who collectively own approximately 32.5% of the Company, have all tendered their shares into the offer so that Thomson Reuters now owns approximately over 32.5% of FX.

51. Under the terms of the Merger Agreement, upon consummation of the Proposed Transaction, Merger Sub will merge with and into FX, whereupon the corporate existence of Merger Sub will terminate and the Company will continue as the surviving company in the Merger.

52. The Company press release announcing the Merger Agreement stated, in pertinent part:

This transaction brings together two leading companies in their respective segments of the dynamic foreign exchange marketplace, one of the largest and most liquid asset classes. [FX] and Thomson Reuters have complementary customer bases and long standing relationships with bank liquidity providers.

Thomson Reuters is a key provider of access to market liquidity and workflow solutions to the inter-bank electronic FX markets. Participants in the FX market use Thomson Reuters to access content and pre-trade analytics, connect to their counterparties, find liquidity and trade in regulatory compliant and secure environments.

* * *

“[FX] will now have a bigger stage from which to drive greater innovation and growth, with access to Thomson Reuters global reach, standing in the FX community and focus on client solutions,” said Phil Weisberg, chairman and chief executive officer, [FX]. “The combined platform allows us to deliver greater value to our clients and employees, building upon the foundation that we have established over the past twelve years. In addition, we believe this is a compelling transaction for our shareholders.”

53. FX has said that its own platform aimed at servicing companies and investors will merge with Thomson Reuters’ traditional platform focused on bank-to-bank currency-trading systems, though the Company has declined to give its shareholders additional details until after the completion of the Proposed Transaction.

54. According to a Thomson Reuters representative: “The details of the combined organization will be reviewed as part of the integration planning activities and any announcements will be made after the close of the transaction.”

The Proposed Transaction Undervalues the Company

55. The Merger Consideration offered to FX shareholders in the Merger Agreement does not represent the true value of the Company and is unfair and inadequate, particularly at a time when FX’s business is steadily strengthening and growing.

56. By selling the Company at this inopportune time for the inadequate price of $22 per share, Defendants are wresting away the opportunity for public shareholders to enjoy the benefits of their investment. In fact, within the brief five months as a publicly traded company, FX’s stock reached a pre-deal high of $18.72 per share, 56% more than its IPO price. Furthermore, FX has significantly outperformed the New York Stock Exchange Composite Index, which tracks all common stock listed on the New York Stock Exchange, as illustrated by the chart below:

57. Shares in the Company have been in record demand despite the volatility of the markets. On July 6, 2012, the last pre-announcement trading date, the Company reported that its total daily average trading volume of FX shares for June 2012 was a record $98.6 billion, a 10% increase from both the previous month and from June 2011.

58. The inadequacy of the Merger Consideration is obvious when the Proposed Transaction is viewed in light of other comparable transactions. For example, even the median multiple for the precedent transactions examined by the Company’s financial advisor results in a value of $27 per share, much higher than the $22 per share Merger Consideration being offered here.

59. Furthermore, the Company’s shares have been mostly trading at, or above, the offer price since the Proposed Transaction was announced, reaching an all-time high of $22.50 on July 18th. There have even been days where the lowest traded price for the day was above $22 per share Merger Consideration. Obviously, the market believes that $22 is not a fair price and there is some expectation that a higher price could be on the way.

60. The gross inadequacy and unfairness of the Merger Consideration is further demonstrated by FX’s strong financial condition and business prospects.

61. As recently as May 3, 2012, in announcing FX’s financial results for the first quarter of 2012, Defendant Weisberg touted the Company’s value: “Our first quarter results reflect the continued strength of our platform and the investments we are making to maintain our leadership in the electronic institutional foreign exchange market.”

62. Weisberg elaborated further: “The increase in our volumes during the quarter amidst a volatile market environment highlights the depth of our relationships globally and the quality of our product. I would also like to recognize the entire team at [FX] following the successful completion of our recent IPO.”

63. Recently reported developments are perhaps most indicative of the Company’s promising future for long-term growth. Among the highlights of the reported financials, the Company announced that total revenues for the first quarter of 2012 had increased 10%, to $30 million, compared to the same period for the previous year. The report attributed the increased revenues to stronger transaction fees, as well as to user, settlement and license fees.

64. FX further reported increases in earnings per share and total average daily trading volume. The Company, which for purposes of gauging trading volume counts only one side per trade, saw its average daily trading volume swell to $86.8 billion, up 13% from the first quarter of 2011.

65. These announcements foreshadow FX’s bright future. In its Form 10-Q filed with the SEC on May 8, 2012, the Company stated, in pertinent part:

Key Operating Metrics

We believe that there are two key variables that impact the revenues earned by us:

| ● | the volumes that are transacted on our platform; and | |

| ● | the amount of transaction fees that we collect for trades executed through the platform (which are a result of our pricing tiers and the mix of contracts that we transact). | |